2021 In Review

2021 In Review

Equity markets in the second year of COVID-19.

Dear reader,

Thank you for subscribing to my newsletter. I’m very grateful for your support and wish you an amazing 2022 (even with the pandemic overhang). You can expect more of the same content going forward, and as always, feel free to leave your comments or email me.

Kind regards,

JL

In terms of returns (dividends included), the U.S. S&P 500 led the way last year, producing a gain of 29%. The Nasdaq came in second, returning 28.4%, whilst the Europe 600 index brought in 16.7% (all in USD, with reinvested dividends). Not much of a difference there.

Regarding valuations, the Nasdaq commands a relatively extreme P/E ratio of 40, which is to be expected based on its speculative growth composition. The S&P stands at 26.3, and Europe appears cheapest, with an earnings multiple of 20.8.

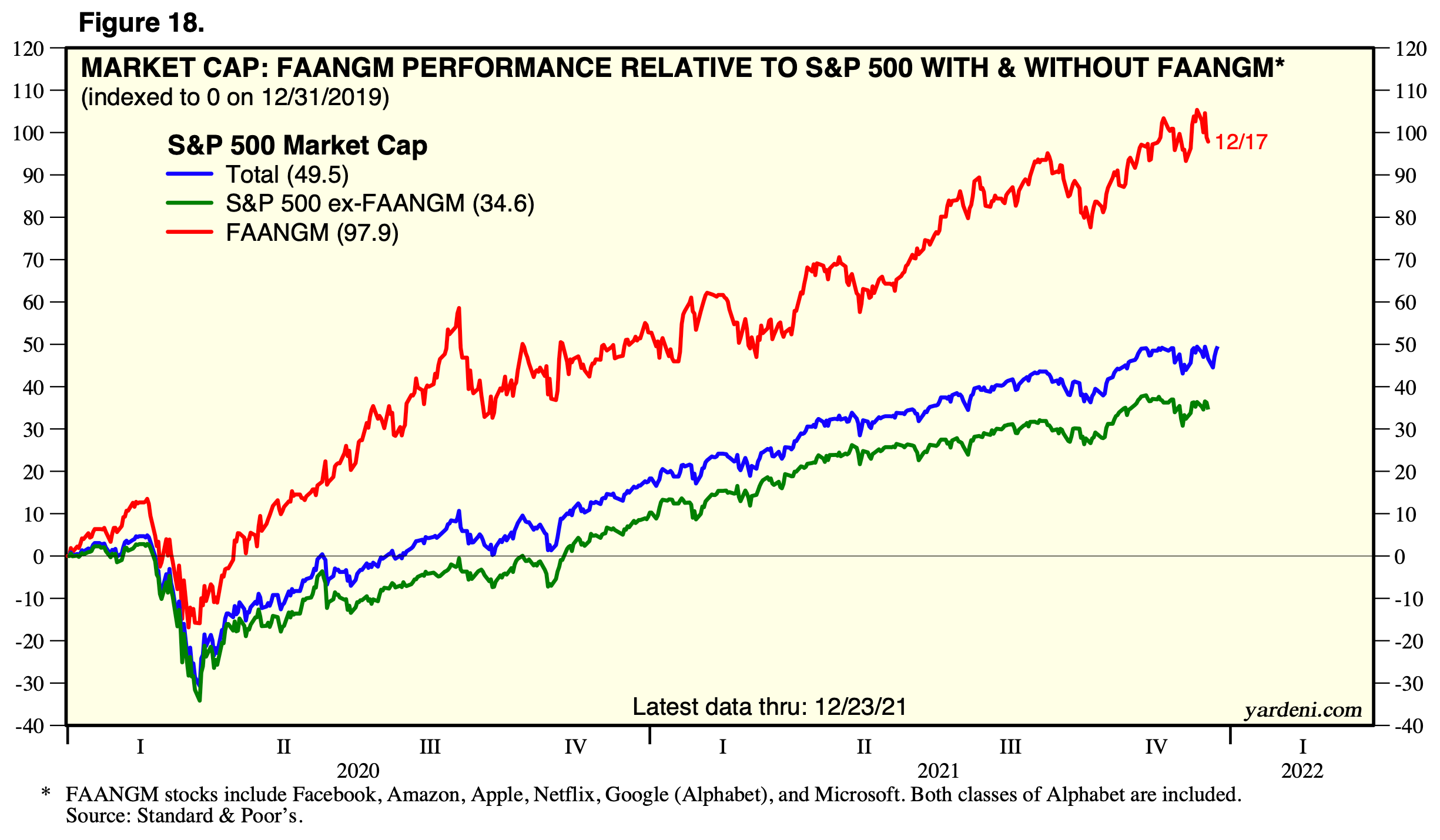

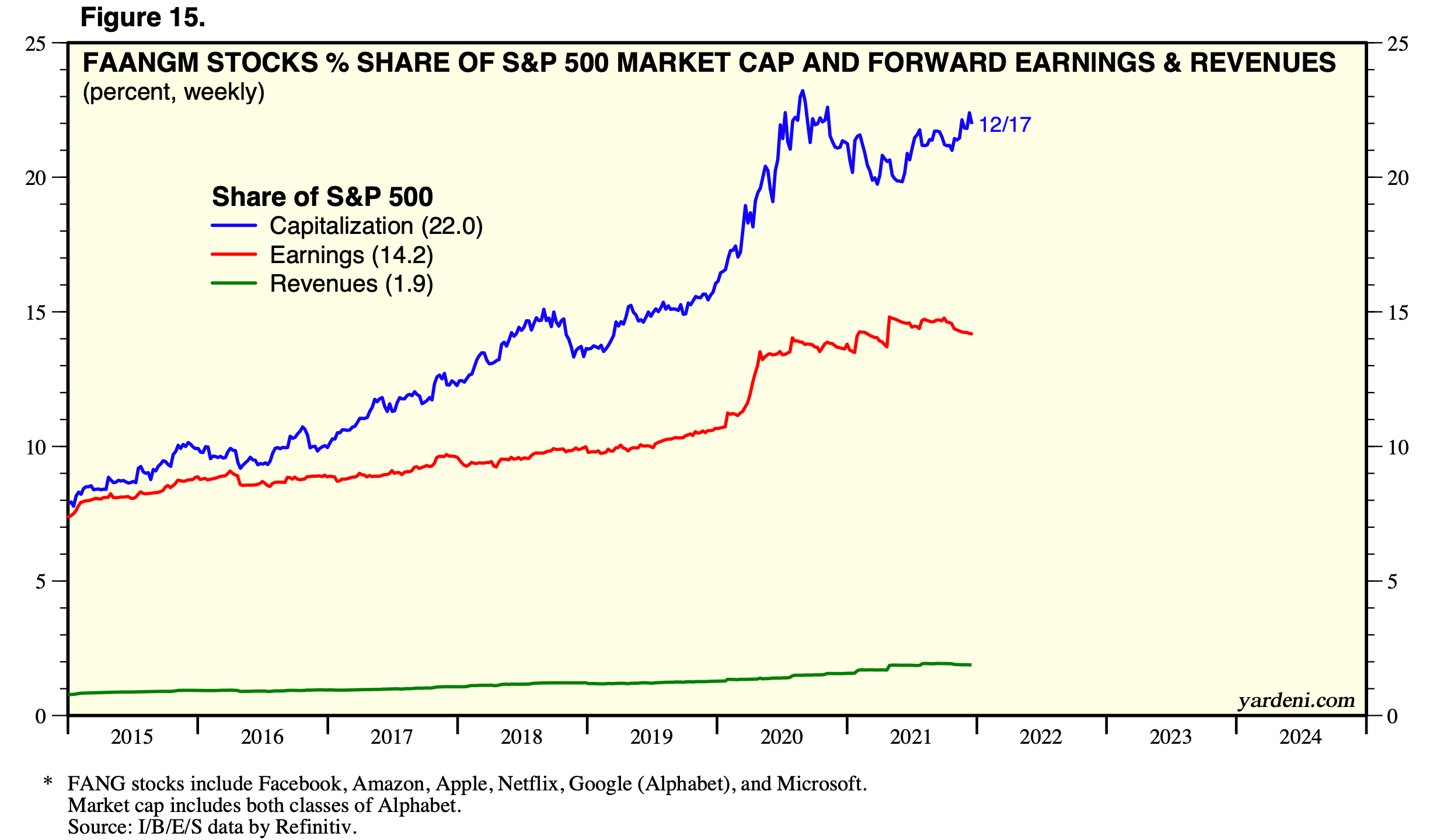

This is not an original thought, but we should keep in mind that looking under the hood of an index can be quite revealing. The S&P 500’s performance, for instance, continues to be driven by the FAANMG group, which includes Facebook, Amazon, Apple, Netflix, Microsoft, and Google; America’s role models of corporate success.

Indeed, the graph below shows that extracting this group from the S&P would have reduced the index’s return in the past two years by about 15%; on its own, the group doubled in value during this time.

If you want more food for thought, consider that FAANMG also comprise about 22-24% of the market-cap weighted S&P 500 index and account for roughly 14% of constituents’ total earnings (Yardeni Research).

Moving on to the elephant in the room, let’s analyse China’s markets in 2021. Subscribers will be aware of the Evergrande collapse and the state’s regulatory crackdowns through my Market Mayhem newsletters, and these events certainly took their toll on stock returns.

The CSI 300 index, which tracks 300 mainland firms that have their Class A shares listed on the Shenzhen and Shanghai stock exchanges, is down a minor 3.5%. In contrast, the Hong-Kong-based Hang Seng Index slid 14.8%, and the Hang Seng Tech Index suffered disproportionately, with a loss of 34.7%. All returns are based on Chinese Yuan and include dividend reinvestments.

The selloff is reasonable if we consider the extreme risk of the Chinese government’s interference in the economy and markets; after all, the state practically killed the entire private tutoring industry in a single move, and equities are risky enough in themselves. Naturally, others argue that this is a passing wave of regulation that has made stocks in a growing economy with a massive home market extremely cheap. Indeed, the Hang Seng Tech Index trades at a P/E of only 14. I’m staying away from China because the situation is subject to too many unknown variables, but that doesn’t mean you should.

Globally, those markets that we tactfully label ‘developed’ - such as those of those of the U.S., UK, Germany, etc. - have produced a collective return of 22.6%, as per the MSCI World Index (P/E of 23). ‘Emerging’ markets - which include Russia, Turkey, Brazil, etc. - did not perform nearly as well, dropped 3.2%, and are now at an earnings multiple of 14.

Inflation was a hot topic in 2020, and also in 2021. The pandemic essentially froze the economy for a time, and the subsequent reopening coincided with record money printing programs and supply chain issues. The most recent U.S. CPI reading came in at 6.8% for all items, and 3.94% excl. food and energy. For the Euro Area, the Harmonised Index of Consumer Prices (HCPI) stood at 5%, and let’s not mention Turkey. In the face of this depreciation and record low interest rates, cash was trash, and it made sense that equities rallied due to inflows.

Now, the scene is different. Central banks have pivoted from the ‘transitory inflation’ stance to action, with the Fed and ECB planning to slow their bond purchases throughout 2022. The former is even set to raise rates three times. That’s bad news for stock returns, since the enhanced appeal of alternative investments makes the cash flows from equities worth less, depressing valuations - that’s the theory, anyway.

Also, without going on too much of a tangent, let’s examine how gold did this year. It didn’t go anywhere. The traditional haven asset which typically rises in value in times of uncertainty - and inflation - disappointed investors with a loss of 4.3%. Maybe it has been replaced by Bitcoin.

In 2021, firms raised more capital through equity financing than ever before, at a total of $1.4 trillion - $1,400,000,000,000 - according to Bloomberg.

Tencent topped the list, bringing in about $14.7 billion, followed by Rivian (an EV manufacturer) at $13.7 billion, and LG Energy at $10.8 billion.

It all makes sense. As mentioned, equities were the only attractive asset class of the past two years, and valuations were therefore stretched. That means more bang for your buck from the perspective of capital-hungry public companies.

Altogether, 2021 was not at all what I expected - I thought the market would be down based on the craziness I saw in the last quarter of 2020. The hammer might drop next year (or not, nobody knows).