Market Mayhem (13/11/21)

Market Mayhem (13/11/21)

Evergrande, Fractured Conglomerates, Inflation, and EVs.

China Update

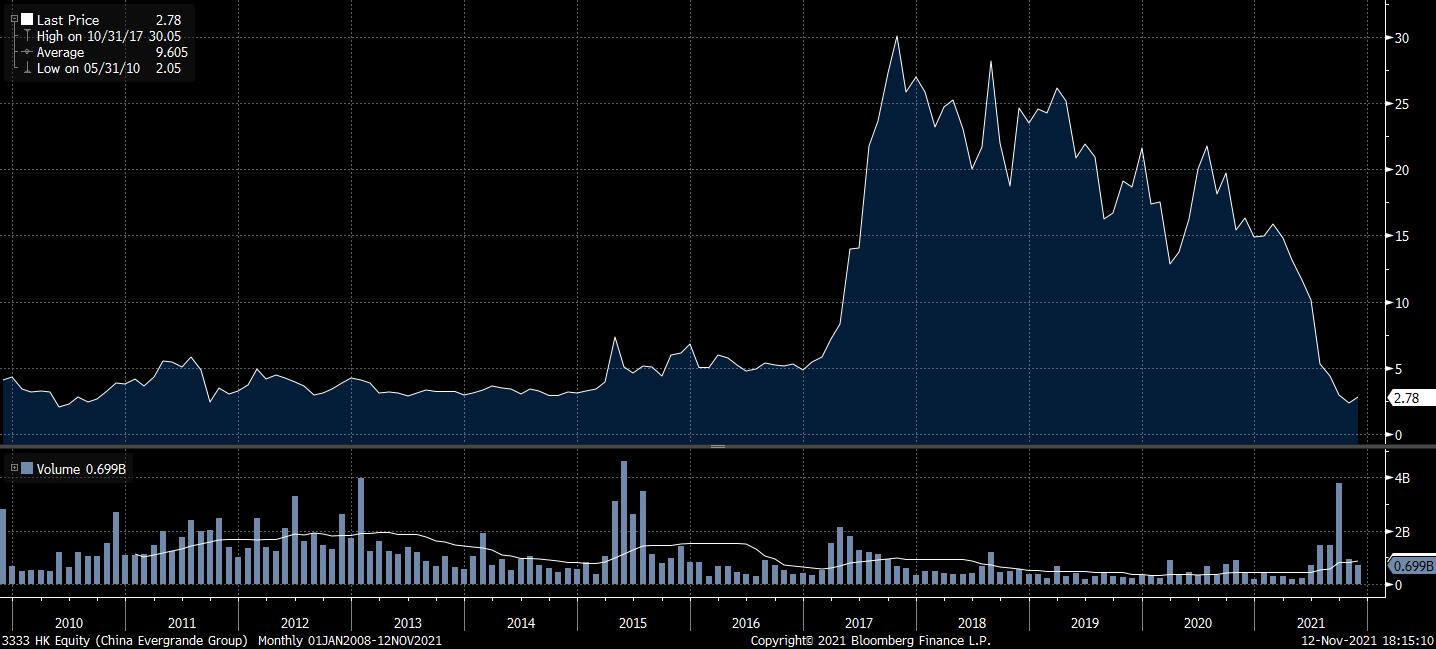

The Evergrande crisis seems to have disappeared from the headlines. Obviously the media has moved on, yet the situation remains extremely precarious. Here’s a quick recap.

China Evergrande Group’s core business is the development of residential real estate. It is also an investment holding company with exposure to a variety of firms operating in the hotel, professional sports, mineral water, and health industries, among others.

It owes a smorgasbord of creditors, including banks, foreign creditors, local investors, and homebuyers, who paid in advance for approximately 1.6 million of properties that the firm is unlikely to complete.

As of June 30th, 2021, Evergrande faced ~$89 billion in debt, and held a measly ~$14 billion in cash.

The reported value of total current assets (the most liquid) was ~$305 billion and total liabilities stood at ~$302 billion. Deducting liabilities from current assets leaves us with a fire sale value of ~$3 billion, meaning that those liabilities could be covered - in theory.

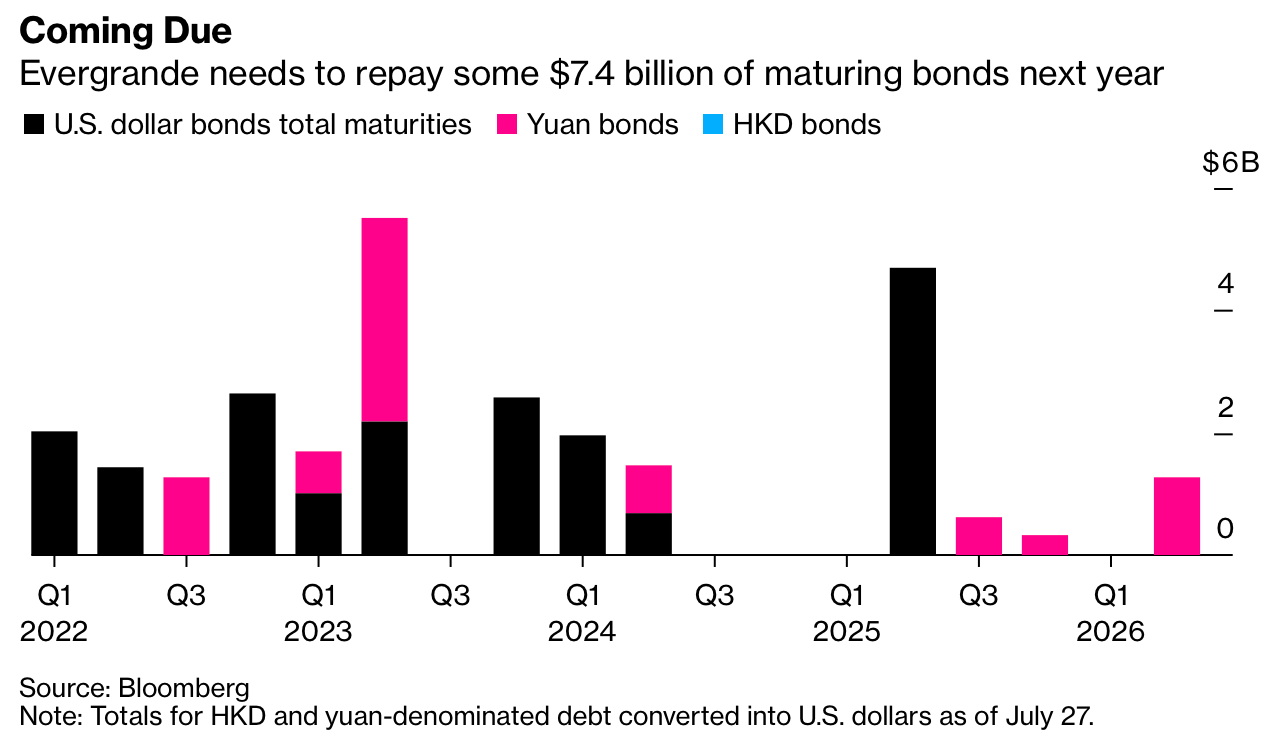

However, Evergrande’s survival is dependent on its ability to raise a mountain of cash, and quickly. It doesn’t help that 2/3 of current assets are comprised of inventory. The firm needs to repay $7.4 billion in principal next year, plus coupon payments on offshore debt of ~$1.7 billion.

The clock is ticking, and Evergrande’s potential collapse does not only threaten investors. Chinese real estate makes up 30% of GDP and residential real estate comprises 17%. Chaos in China would likely ricochet internationally as the worlds financial systems and economies are intricately connected.

No-one knows whether there will be a government bailout, although Ashmore Group, BlackRock, FIL, and UBS evidently think this is a contrarian opportunity - these asset managers have actually invested in Evergrande’s debt.

On a related note, Chinese stocks seem to be making a recovery from recent selloffs. This week, the CSI 300 rose ~2.3%, and the Hang Seng index ticked up by ~2.8%. Personally, I’m still thinking about whether this is an opportunity or a trap. I don’t understand Chinese culture and would like to avoid extra governmental risk, but the growth opportunity for certain firms like BABA is definitely tempting.

Fractured Conglomerates

Since 2000, investment banks raked in ~$7.2 billion in fees supporting the formation of the General Electric conglomerate. The firm is now planning to break up, which will please those banks further still.

GE’s healthcare division will be spun off in 2023, with GE retaining a 19.9% stake. GE Renewable Energy, GE Power, and GE Digital will be moulded into a single energy-focussed spin-off in 2024. The original GE will set its sights on the aviation business. All three will have investment-grade credit ratings.

GE ran into serious trouble during and after the financial crisis, and even sought a bailout by Warren Buffett at the time. The firm has been plagued by inefficiencies and has locked up shareholder value ever since. The divisions are likely to trade at higher valuations once they are separated. I anticipate that they’ll be lean and mean, like a sports car with stripped interiors.

Johnson and Johnson, the world’s largest healthcare company, plans to spin off its consumer products division within 18-24 months via a stock offering. The unit produces Band-Aids and Baby Shampoo, among others, and is forecast to bring in $15 billion in sales this year.

“[The spin-off] will allow J&J to focus on delivering industry-leading biopharmaceutical and medical device innovation and technology” - Alex Gorsky, CEO

Also…

“[The new company will be] a global leader across attractive and growing consumer health categories” - Alex Gorsky, CEO

Nonetheless, for all the hype, J&J seems to have some skeletons in its closet.

Toshiba, a Japanese industrial conglomerate, may also be on the cusp of a breakup. Shareholders must still make the decision at an extraordinary meeting in March. If approved, the actual three-way split would likely be completed in 2023.

Company A would house Toshiba’s infrastructure, nuclear, and heavy engineering operations plus those involving sensitive technology like AI and quantum computing. Company B would comprise asset management operations, and Company C would specialise in semiconductors and other electrical devices.

Toshiba’s shareholders have shown a prolonged pattern of discontent relating to the company’s persistent ‘conglomerate discount’ and other controversies.

Inflation Concerns

The October U.S. CPI rose to 6.2% year on year. Excluding food and energy - the most volatile components - the figure stood at 4.6%. In Germany and the UK, the Harmonised Index of Consumer Prices rose to 4.06% and 3.02% YoY, respectively.

Should you be worried? No.

“For a piece of information to be desirable, it has to satisfy two criteria: it has to be important, and it has to be knowable.” - Warren Buffett

It may be important, but nobody knows whether inflation is transitory or ongoing. There are solid arguments for both sides, but the information is simply not desirable to the long-term investor.

The cartoon below illustrates classic market irrationality.

EVs and Capitalist Populism

Rivian, an EV manufacturer, listed on the Nasdaq this week. The firm raised $11.9 billion, which constitutes the highest IPO haul for a U.S. firm since Facebook’s IPO in 2012.

Rivian is now worth $111 billion. It also produced 12 vans this year and brought in a stunning ~$1 million in revenue last quarter. Nothing new here.

The firm is backed by Amazon, which expects 100,000 delivery vehicles from Rivian by 2030 and holds a 20% stake, which is surely a vote of confidence.

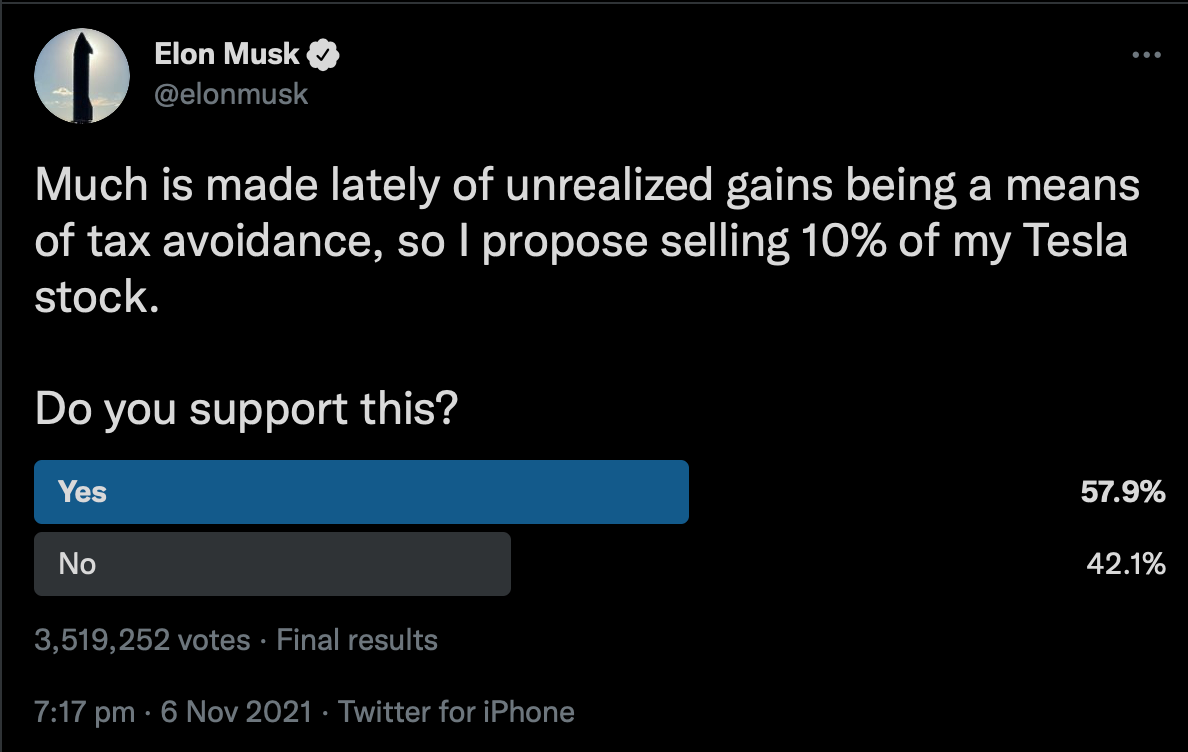

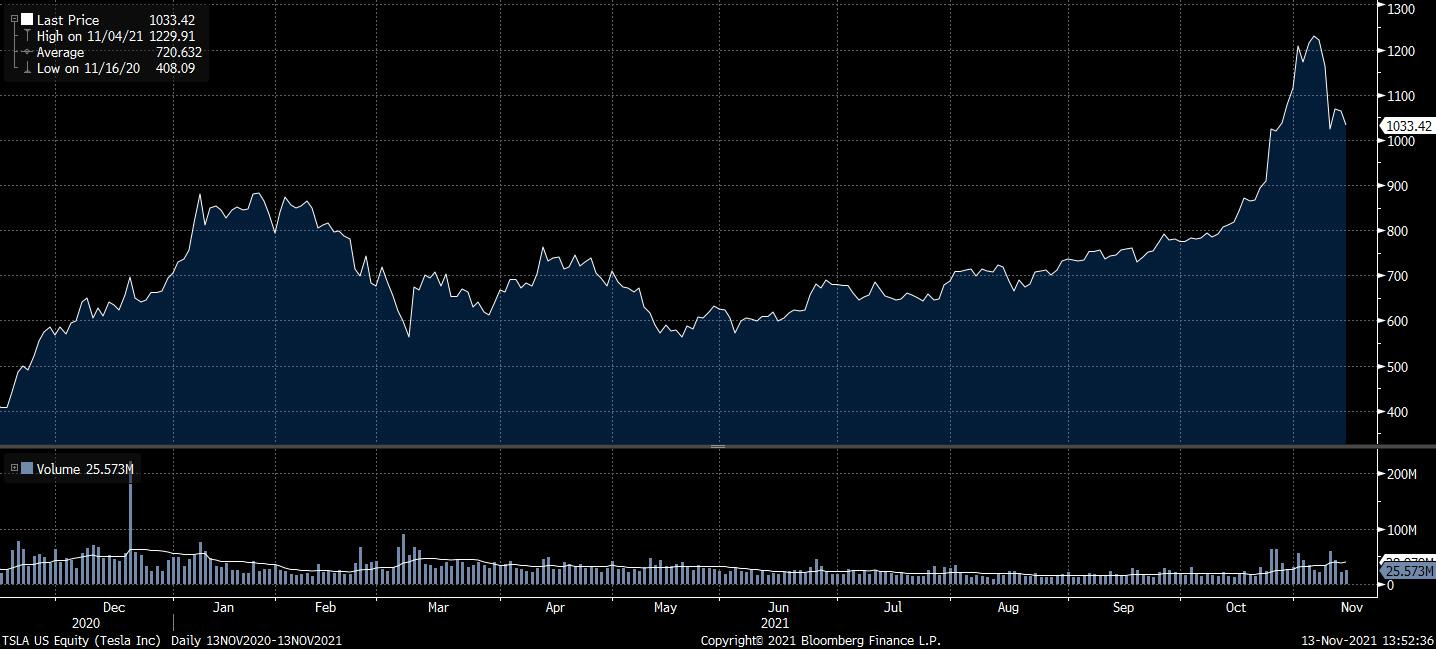

Elon Musk made another Twitter announcement.

Maybe he’s trying to show that he’s in touch with the people, but the shareholders were not happy. Musk is Tesla, and it seems that the sale was interpreted as a loss of faith by current shareholders, who sent the stock down 10-15% over the course of the week.

That’s it for this week. I decided to exclude COP26 as I’m deeply skeptical of any ‘on paper’ agreements that may have been reached there. I’ll check back in when there’s tangible movement that is worth reporting.