Market Mayhem (18/12/2021)

Market Mayhem (18/12/2021)

In focus: Inflation and Central Banks, Erdoganomics, Reddit IPO, and Bonus Time.

Not so transitory after all?

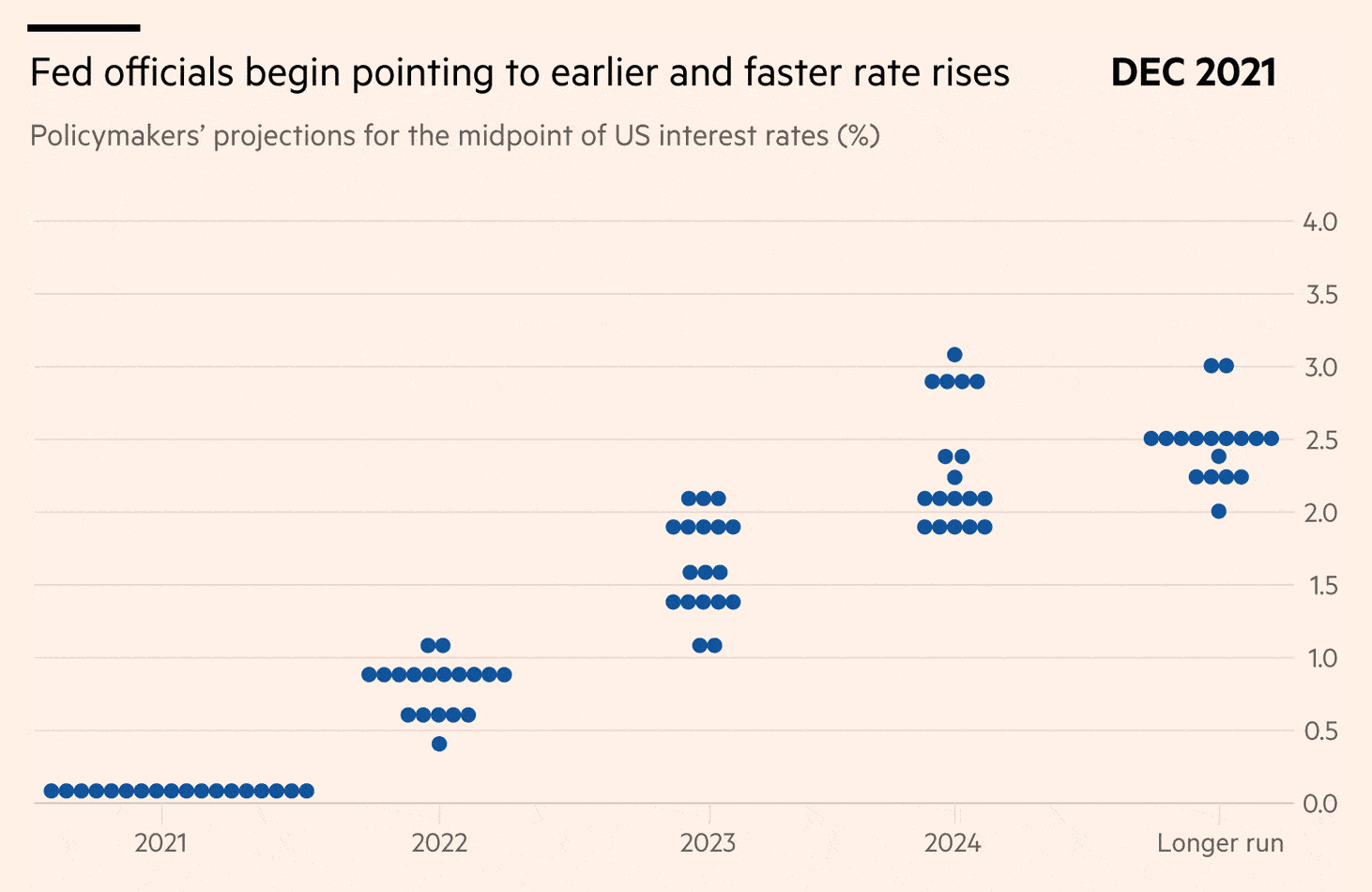

The Fed is turning hawkish. In a meeting on Wednesday, chairman Jerome Powell declared inflation to be the primary threat to the U.S. economy, and announced certain countermeasures.

Indeed, accelerated tapering is scheduled to begin in January 2022, with monthly bond purchases being cut by $30 billion instead of $15 billion. This means that stimulus will be entirely absent by March 2022. Further, three rate hikes are expected next year, followed by three more in 2023, and two more in 2024. In the meantime, rates will remain the same at 0-0.25%.

Historically, interest rates are negatively correlated with stock valuations i.e., as rates rise, valuations fall, and vice-versa.

This effect can be seen below, where the U.S. 10-Year Treasury Yield in % (also known as the risk-free rate, since governments very rarely default) is laid over the price of the S&P 500.

There’s a simple explanation for this relationship. In essence, investing involves putting up a lump sum now in expectation of future cash flows. The value you assign to those cash flows depends on the appeal of alternative investments. For example, if the risk-free rate stands at 15%, it would be foolish to pay 35 times earnings for a company. That’s because the risk for that bond is near-zero - in contrast to a company’s equity - but the cash flows are still formidable.

The bottom line: investors will assign less value to a firm’s future cash flows if rates are high, and more value to it if rates are low.

If you won’t take it from me, take it from the master himself, Warren Buffett:

“Interest rates act like gravity on [stock] valuation”.

“The most important item over time in valuation is obviously interest rates. If interest rates are destined to be at very low levels… it makes any stream of earnings from investments worth more money. The bogey is always what government bonds yield until maturity.”

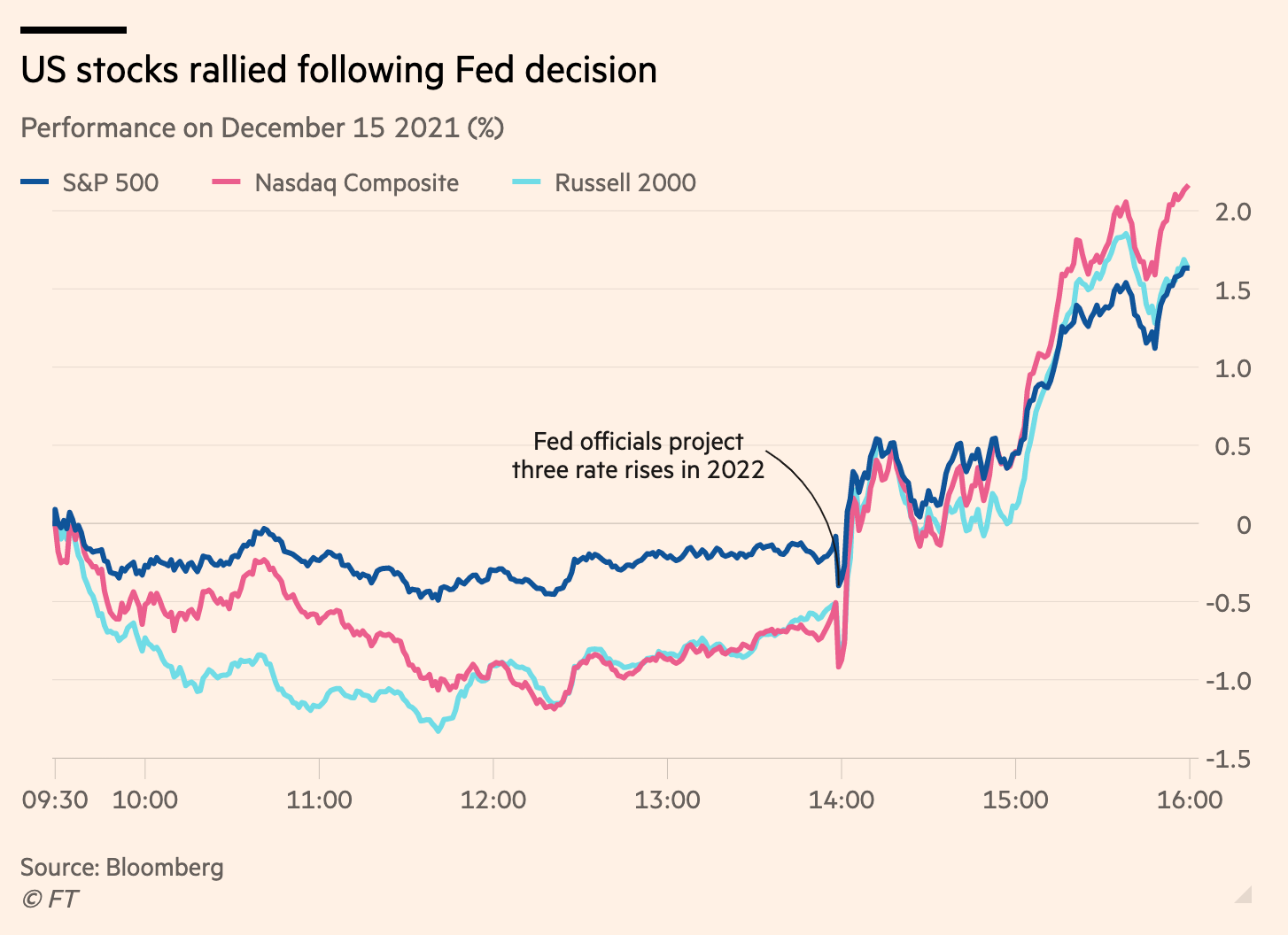

Despite this, the market shot up after Powell’s announcement in another seemingly illogical move typical of this market.

Maybe traders took comfort in the fact that Powell seemed to be aware of the inflation situation - who knows.

The ECB wants to wane the Eurozone off stimulus too, but at a slower pace.

Christine Lagarde announced that the €1.85 trillion Pandemic Emergency Purchase Programme (PEPP) launched this year would reduce net buying next year and cease altogether in March.

However, an older scheme - the Asset Purchase Programme (APP) - would continue pumping money, and at an increasing rate. Q1 monthly purchases of €20 billion will jump to €40 billion in Q2, and €30 billion in Q3. Purchases will continue at €20 billion come Q4, ‘for as long as necessary’.

Regardless, in the next few months and years, we should certainly get ready for Mr. Market’s mood swings.

Erdoganomics

Turkey’s president is still busy mixing an explosive economic cocktail; on Thursday, the central bank further lowered rates from 15% to 14%, despite annual inflation of 21.3%. The minimum wage was also bumped up by 50%, which may drive a feedback loop.

That’s not all. Perhaps to protect their wealth, Turkish citizens have plowed money into the stock market, driving the Borsa Istanbul 100 index up 46.7% (26.4% in real terms) in the last 12 months. However, in Dollars, the index is actually down 33%.

Erdogan may assume that a devalued Lira will benefit the country’s exporters, but that’s only partly true. Turkish firms with international operations, such as airlines, defence groups, and carmakers, can bring in foreign currency denominated revenues but still pay their local staff in Liras. For other firms, the situation is simply dangerous; input costs have risen by 54% in the last 12 months, but products are becoming cheaper by the day.

Also, on Friday, the Turkish market went nuts and lost 8.5%, triggering circuit breakers which suspended trading for a while. This move breaks with a prolonged trend of index appreciation accompanied by the Lira’s devaluation. Below you can see the performance of the index (right axis) alongside the Lira to USD FX rate (left axis) over the last 12 months (click to enlarge).

Compared to the start of 2021, it now takes more than twice as many Liras to purchase a single U.S. dollar - an all-time low. As always, this crisis will disproportionately punish the poorest, and 40% of Turks earn the minimum wage. The wealthy, on the other hand, likely flipped their riches into U.S. dollars quite some time ago. I bet Erdogan is among them.

Reddit Is Going Public!

The popular online discussion forum, which sprung to prominence with the WallStreetBets frenzy in January, has filed for a listing with the SEC.

The firm was valued at $10 billion in a funding round in August, but as of now, there is no information as to how many shares will be sold or the target valuation that Reddit will seek.

Newly crowned as a ‘haven for free speech’, Reddit is gearing up to build an advertising business to drive profit. This contrasts with its current state, where users only have the option to purchase on-platform awards that can be given to users for posts and comments.

To me, it seems that management will have to strike a fine balance between effectively monetising the platform and preserving its open, user-friendly nature. I’m quite the fan, so I hope they succeed.

Mo’ Money Mo’ Problems

Goldman Sachs and JP Morgan are preparing to supersize their investment banking (IB) bonus pools by 50% and 40%, respectively, as bankers prep for champagne showers.

The reason, according to James Dobkin, a veteran who spent nearly half a century at Goldman Sachs, is that firm’s want to retain their star players:

“You are paying for retention and not just paying for performance.”

“This year [2021], firms may have to overpay to keep the people they most want”.

It’s been a lucrative, record year for both firms: Goldman Sachs' IB segment racked up about $11 billion in sales year-to-date, whilst JPM brought in nearly $10 billion. IB fees come from advising on public listings, private equity buyouts, debt offerings, and mergers and acquisitions.

Salaries, benefits, and bonuses are a massive expense for financial services firms; in Q3 2021, Goldman Sachs incurred $6.6 billion of operating expenses, of which $3.2 billion comprised compensation.

It seems the grind may have been worth it - at least this year.

Note: I’ve refined this section by recommending only one or two enticing articles and other resources that I’ve stumbled across (quality over quantity). If you find these useful, send me an email, so I can keep doing it right!

Top reads from this week:

The Secret Diary of a Sustainable Investor - Tariq Fancy. An excellent three-part essay concerning the fad of green investing. Written by the ex-Chief Investment Officer of Sustainable Investing at BlackRock.

Elon Musk: Interview with FT’s Person of the Year - Financial Times.