Market Mayhem (20/11/21)

Shell, Turkish Inflation, Unilever's Divestment, & COVID Plays.

Ex-Royalty

Shell has been riding the headlines for a while now. In May, a Dutch court ordered the firm to cut its net carbon emissions by 45% through 2030 relative to 2019 levels. The target exceeded the firm’s own and was perceived as a victory by climate activists. A slap on the wrist for oil majors, who wince at the idea of actually meeting green commitments, was long overdue.

In late October, an activist fund (Third Point) demanded that Shell divide itself into several individual companies, including a ‘legacy’ branch that focused on oil and gas and a renewable energy entity. The activist’s stake was estimated to be worth $750 million, and their letter to the firm’s shareholders stated the following:

“[Shell has] too many competing stakeholders pushing it in too many different directions, resulting in an incoherent, conflicting set of strategies attempting to appease multiple interests but satisfying none”

- Third Point, Financial Times

One of Shell’s largest shareholders publicly disagreed.

“People are fully aware of how difficult it would be to break up Shell.”

“Just because Third Point says it makes compelling financial logic doesn’t mean it will happen.”

- Iain Pyle (Fund Manager at Abrdn), Financial Times

Further stirring the pot, Shell now wants to move its tax residence, headquarters, and senior management from The Netherlands to the UK. In addition, it wants to merge its dual share structure and abandon the ‘Royal Dutch’ seal after 114 years.

The company has always quarrelled with Dutch authorities regarding a 15% dividend withholding tax, which is not levied in the UK. A single, wider pool of shares would also allow the firm to boost share buybacks, which are currently capped at approximately £2.5 billion per quarter, pleasing investors.

“The simplification will make Shell more competitive, it will allow for an acceleration in shareholder distributions and speed up Shell's transition to a net-zero emissions energy business”

- Andrew Mackenzie, RDS Chairman

A vote will be be held on the matter on the 10th of December. The Dutch government has no interest in letting it happen, and has even debated the removal of the dividend tax, yet Boris Johnson will undoubtedly be pleased.

The Turkish Experiment

Turkey’s economy is in serious trouble as a result of rapid inflation. The latest CPI measure came in at an extraordinary 19.9% year-over-year.

It’s no surprise that the national currency has lost value too, and quickly.

There are several causes, ranging from global factors like supply chain disruptions and higher oil and gas prices, to liberal Turkish monetary policy. Small businesses are being hit the hardest, as they have a reduced capacity to pass on rising costs to their customers and do not wish to lose business. Per Ahmet, a Turkish carpenter working in Ankara (Financial Times):

“Input costs have gone up so much that we cannot keep up with them”

“Just before the pandemic, chipboard — our main input — was 94 lira [per panel]. Now it’s 380 lira.”

Turkish producer prices have risen by 46.3% year-over-year, which is more severe than in any other country and almost double the rate of Russia, at 25%.

Economic orthodoxy would demand that the central bank raises interest rates to curb inflation. However, Erdogan believes that higher rates are the cause of inflation, which is a unique idea.

In fact, Turkey’s one-week repository rate has been adjusted three times, from 19% at the start of September to 15% currently. South Africa and Hungary have raised rates, and Western central banks such as the Fed are actively curtailing their quantitative easing programmes.

It’s perplexing to me that Erdogan is so willing to throw gas on the fire. His political opponents are sure to make use of it. The whole story sounds eerily familiar…

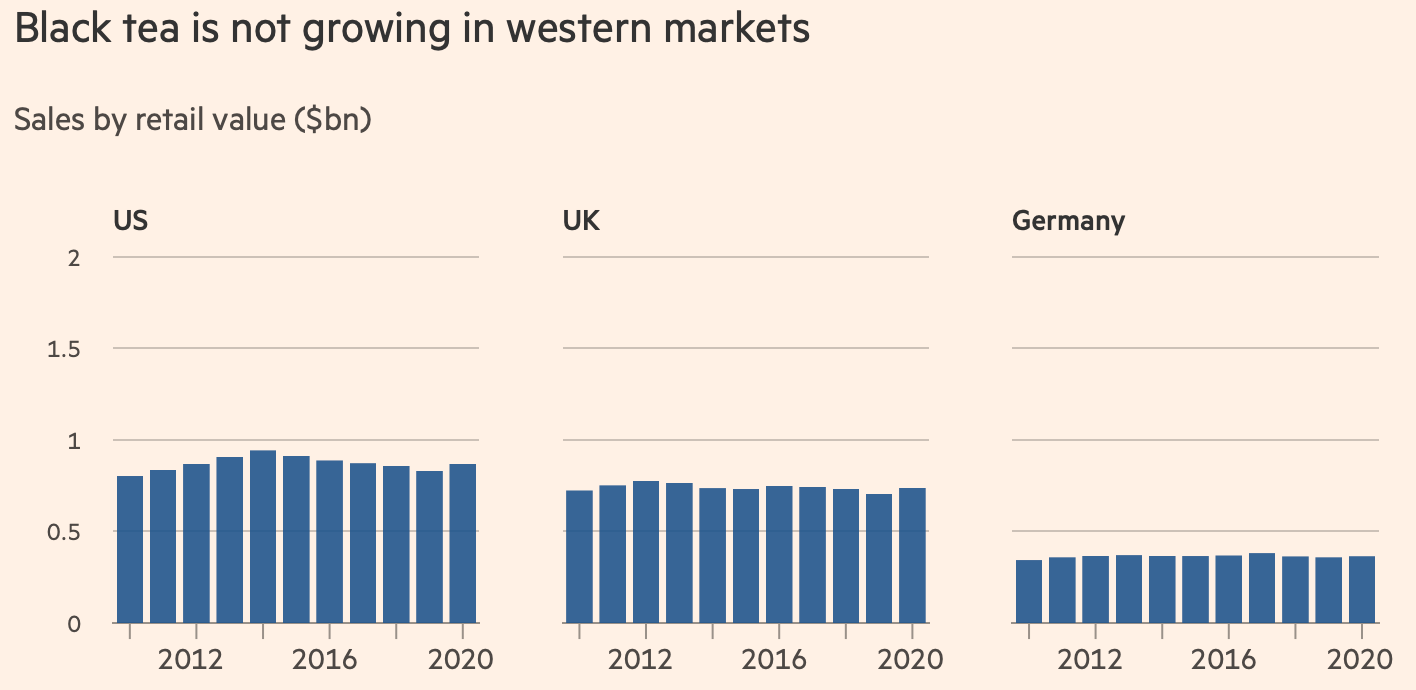

Unilever Divests Itself From Black Tea

CVC Capital Partners has won a bid to purchase Unilever’s tea division, named Ekaterra, which includes the PG tips and Lipton brands. The price tag is a steep €4.5 billion on a debt-free and cash-free basis, and the deal will complete in H2 of next year.

Like the tobacco business, the tea industry has a dark reputation of human rights abuses and marginal pay. The Kenyan operation is also facing legal clashes relating to ethnic violence in 2007.

Beyond ESG concerns, black tea consumption is also dwindling in Western markets, as consumers prefer coffee, herbal tea, and kombucha - the hipster’s favourite.

However, Unilever will retain operations based in Indonesia and India, where consumption of black tea is rising.

The sale follows activist pressure and dissatisfaction with management - an investment in Unilever has been dead money for the best part of 5 years. Since 2016, there’s been no revenue growth, and operating profit has increased only slightly.

The Early Bird Gets the Worm

A random thought crossed my mind the other day: as value investors, we are skeptical of prevailing trends and analyse valuations carefully, but would it have paid off to get in on pandemic trends earlier than anyone else?

In other words, how have those investors fared that purchased the stocks of vaccine companies?

It would have been an absolute bonanza.

Between the 1st of April 2020 and now, Moderna returned almost 800%, with BioNTech - the firm that collaborated with Pfizer - bringing in 440% before transaction costs. Meanwhile the S&P 500 outperformed the other firms and almost doubled.

What about airlines?

In this case, things were less lucrative - the S&P, which is relatively diversified, outperformed all of these firms.

In hindsight, it seemed obvious that the vaccine firms were worth betting on as part of a wider basket, despite there being no guarantee that they would produce a successful shot - the case of CureVac, which was in the race before ultimately failing, comes to mind.

“Be fearful when others are greedy… and greedy when others are fearful.”

- Warren Buffet

I have no regrets. Back then, I had no capital to invest anyway, but I could view the entire spectacle from the sidelines and related to the uncertainty and fear that many investors felt. The world keeps spinning, and it takes courage to take advantage of discounts, which I’ll keep in mind going forward. Maybe the market will crash just in time for Black Friday? It wouldn’t be surprising.

A few other things I’ve been reading and listening to this week:

“Genetic engineering: why some fear the next pandemic could be lab-made” (Financial Times)

“What does COP26 mean for investors?” (Financial Times)

“Florian Schuhbauer and Klaus Roehrig - Applying Activist Tactics to European Markets” (Value Investing With Legends; Columbia University)

“John Deere: Centuries of Farming Innovation” (Business Breakdowns)