Embecta (EMBC)

The world's leading producer of insulin injection devices is available on the cheap.

The Spin.

Becton Dickinson (BDX) - a very large medical tech firm - spun off 100% of its shares in the diabetes care business Embecta (EMBC) to shareholders on the 1st of April 2022. The distribution ratio was 1 share of EMBC for every 5 shares of BDX. EMBC took on $1,650 million of debt as part of the separation, $1,440 of which was sent to BD.

Diabetes and EMBC’s business.

Diabetes is a serious, chronic health condition for which there is no available cure. It is quite common, with the International Diabetes Foundation (IDF) having estimated that, worldwide, there were 537 million adults with diagnosed and undiagnosed diabetes in 2021 (this translates to a circa 9% prevalence rate). To understand diabetes, we need to understand the peptide hormone insulin. Insulin is produced in the pancreas and enables glucose (obtained from food) to enter our cells and excess glucose to be stored as glycogen in the liver for later release. Abnormalities related to insulin are the hallmark of diabetes and can cause hyperglycaemia (high blood sugar), with all the associated negative health consequences.

There are two distinct forms of diabetes. In T1 diabetes (5-10% of cases), the immune system attacks its own pancreatic beta cells, either reducing or eliminating natural insulin production. Hence T1 diabetics are said to be insulin-dependent, and injections are required on a daily basis. In contrast, In T2 diabetes (90-95% of cases), which is the acquired form (think fast food consumption, no exercise, etc.), insulin is still produced, but a resistance to its mechanisms manifests. In the initial decade post-diagnosis of T2, management and treatment methods include diet or lifestyle changes, oral medications, and non-insulin injections like GLP-1 receptor agonists.

But T2 is progressive, and the extreme stress on pancreatic cells to produce more insulin than usual to overcome resistance damages them over time. It is for this reason that a significant proportion of T2 diabetics will - sooner or later - require insulin (about 20%, according to EMBC’s estimates). Once on insulin, T2 diabetics inject the hormone for the rest of their lives.

This means we have the counterintuitive situation where the market for injection devices is in actual fact larger for T2 diabetics (of whom a mere proportion require insulin) than for T1 diabetics (all of whom are insulin-dependent), because the former population is just much bigger in size.

EMBC manufactures and sells insulin injection devices to wholesalers and distributors who, in turn, sell them on to end customers across the globe via acute care hospitals, retail, and other channels. Specific products include pen needles, which are the most common injection device, and are also sterile, single-use, and utilised in conjunction with insulin pens; syringes, which are also sterile and single-use, and used to draw insulin from vials; safety devices, which have shields on both ends of the cannula that prevent needlestick exposure; and other accessories like sterilisation swabs and sharp disposal boxes. Pen needles, syringes, safety devices, and accessories contributed 73%, 15%, 10%, and 2% of sales in FY21, respectively.

EMBC is not too dependent on any one customer, in my opinion. Indeed, 39% of FY21 sales were brought in by the three largest distributors (McKesson, Cardinal Health, and AmerisourceBergen) and 14% of FY21 sales were attributed to the five largest pharmacies. These are all long-term relationships, too. EMBC also offers a diabetes care app, which has seen >400,000 downloads since its launch in 2018 and has >10,000 active users.

Thesis points.

Economies of scale combined with an expansive worldwide sales network, regulation, and IP, insulate EMBC from most competitors. For reference, about 95% of all diabetics who use insulin inject it via pen needles or syringes - as opposed to the 5% who use more expensive subcutaneous pump infusion - and EMBC happens to be the world’s leading producer of these injection devices with a volume-based market share in excess of 2/3. The firm delivered about 7.6 billion injection devices to an estimated 30 million end users across 30 countries in FY21. EMBC presides over three automated and optimised manufacturing facilities located in Ireland, the U.S., and China. The Irish plant has the largest output; it produced 4.7 billion pen needles and 200 million safety pen needles in 2021. In comparison, the U.S. plant put out 2 billion syringes in 2021 and the Chinese site put out 740 million pen needle units.

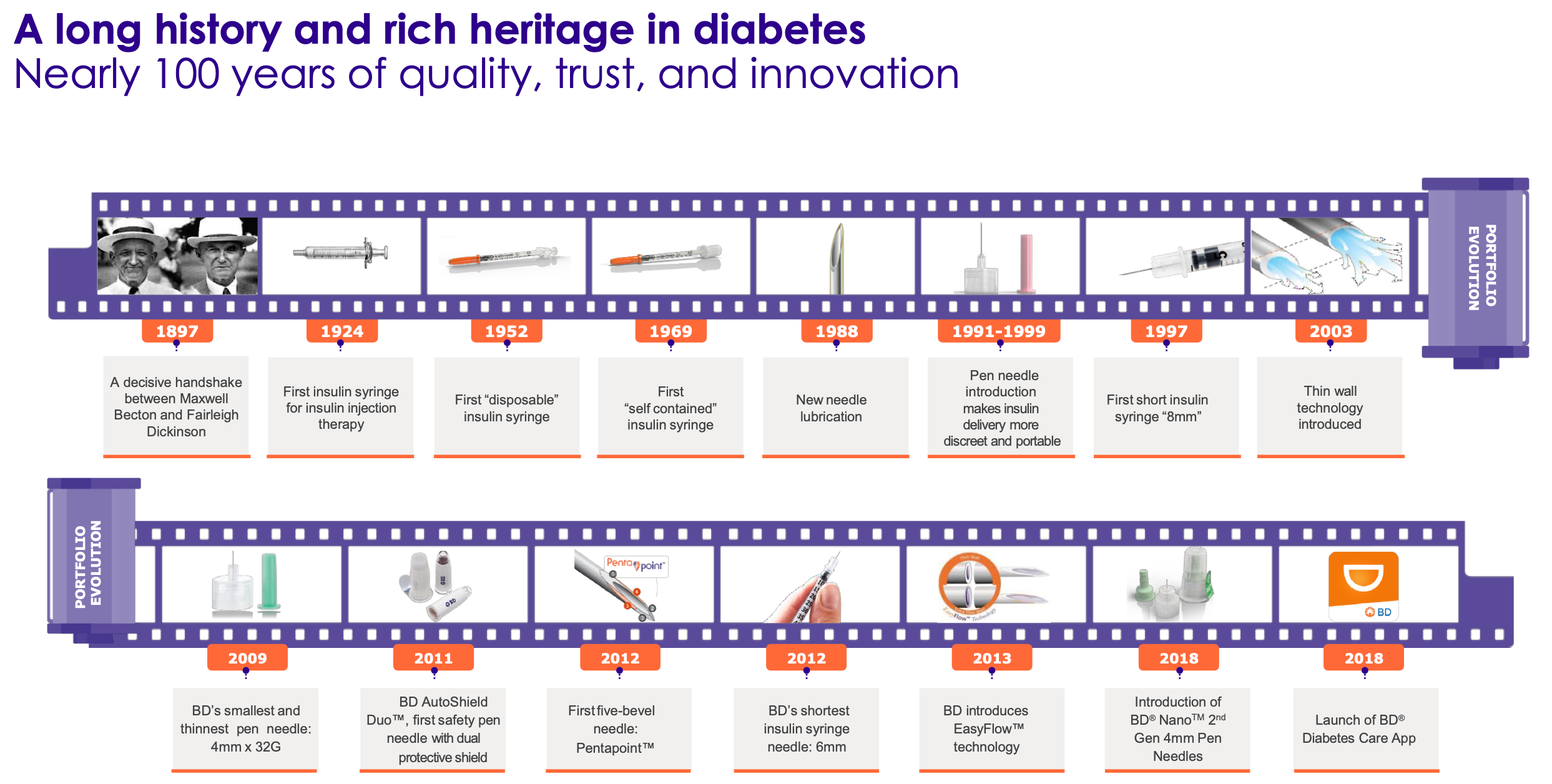

EMBC’s insulin injection business is strongly regulated due to the serious nature of diabetes and high standards for new injection products. New product applications must be reviewed by the Food and Drug Administration (FDA), for instance, just like novel drugs sent for review by biotech companies. Hence established concerns that are reputable and have experience navigating such hurdles - like EMBC, which invented the first insulin syringe in 1924 - could have an advantage over younger market entrants. EMBC also holds an IP portfolio of >2,000 patents relating to its medical devices, plus exclusive rights to some of BD’s IP under special agreements. I believe these three factors are very hard to replicate and work as barriers to entrants in this market, protecting EMBC’s business.

All of EMBC’s ample free cash flow (FCF) was passed up to BD prior to the spin. However, now that EMBC is an independent firm, its management is free to invest $438 million worth of normalised FCF in the business itself, specifically into marketing, bolt-on acquisitions, and more research and development (the improvement of existing products and launch of new ones). The latter area is most promising, as there is a major product in the pipeline. Indeed, EMBC has been working on a closed-loop (automatic, does not require user input), wireless insulin patch pump for insulin-intensive T2 diabetics that promises simple operation, an intuitive interface, low cost (pumps cost a lot more than injection devices), and a larger reservoir.

Pump penetration in the T2 diabetes market is estimated be in the single digits due to complex systems, reimbursement procedures, the necessary training, and a total daily insulin dose requirement. The pump has received Breakthrough Device Designation from the FDA; it could be launched in 2023 and is slated to contribute ‘significant additional sales’. In regard to the numbers, EMBC estimates that there are 280 million diagnosed T2 diabetics across the globe; of these, about 52.5 million (or 20%) require insulin, and in turn, 20 million are insulin-intensive candidates for the pump (7% of the total T2 population). The TAM for this pump has also been estimated at $1.5-1.7 billion by 2030. Of course, digital engagement with and support for the user base is another avenue for growth, and EMBC aims to expand its solutions here. With its independent position and new-found financial freedom, I strongly believe EMBC can rejuvenate its product line and build out its market positions from here onwards.

The trends within the diabetes space favour EMBC. Indeed, aside from the absolute dependence of diabetics on its insulin injection products to avoid drastic outcomes like cardiovascular disease, stroke, and vision loss, the IDF estimates that the total number of diagnosed and undiagnosed diabetics will increase from 537 million in 2021 to 643 million by 2030, and 783 million by 2045. The highest growth in diabetic population sizes up to 2045 is expected in Southeast Asia (68%), the Middle East and North Africa (87%), and Africa (134%). Of course, this makes EMBC’s global manufacturing and commercial reach very valuable. The projected rise of diabetes is also a continuation from the past; between 2010-2018, the U.S. T1 and T2 populations have grown at compounded rates of 5.5% and 4.5%, respectively.

Unless there is some fantastic scientific breakthrough or major disruption, this assures recession-proof demand (yes, we are all concerned) for EMBC’s products in the long-term. The TAM for insulin injection devices is also circa $6-8 billion per annum based on the no. of insulin-dependent diabetics worldwide. EMBC did 1,165 million in sales in FY21, which suggests to me that organic growth without the overall market growth is also possible.

Valuation.

EMBC now trades at an absolute EV/FCF of 6.6x and EV/EBIT of 5.9x. I believe the firm is best valued on an intrinsic basis because a) the multiples of comparable firms are all over the place, and b) their growth trajectories and business characteristics differ too much. Thus, based on an earnings power valuation in which I assumed a simple continuation of the business as is except a 10% compression of the operating margin as a result of increased expenses and investments (as alluded to in the investor presentation), EMBC is worth about $38 per share. I would sell at that price, because I do not believe the success of management’s strategies is guaranteed, and the potential for disruption here seems higher than for SLVM, for instance, due to the attractiveness of this market (think small, nimble medical tech firms). EMBC now trades at circa $27, suggesting a large margin of safety.

Other matters.

The input materials for EMBC’s injection devices include plastic resin, adhesive, needle lubricants, rubber stoppers, packaging, and, above all, cannula (thin intravenous or nasal tubes that allow for medication to be inserted into the body). BD has an agreement to sell cannula to Embecta, and retains all activities and IP related to cannula, its manufacture, and linked technologies. This agreement cannot be terminated until 5 years post-spin, is 10 years in duration, and demands 36 months’ cancellation notice. BD can terminate it at will if there is a change in control of Embecta. The deal has quantity, pricing, and other terms, and there is a ceiling to cannula purchases per annum (demand-dependent). Management is selling the deal as a competitive advantage, but it seems a liability to me.

7 million shares have been reserved for awards under the 2022 incentive plan, which equates to a significant 12% of outstanding shares. Whilst all insiders now own a mere .6% of shares, the CEO, Devdatt Kurdikar, owns 167,630 shares, which would be worth $4.5 million at the current price.

The board has committed to a pay out of 20% of GAAP net income to shareholders.

Catalysts.

Insider purchases and very positive pump announcements.

Disclaimer: this write-up describes the author’s own research and opinions, and does not constitute investment advice, whether explicit or implied. Invest at your own risk and do your own due diligence. I hold a material position in the issuer’s securities.

Spent some time reading through their S10, investor presentation and Q10. Trying to understand the competitive environment around diabetes care.

I don't buy that the company is set up for growth. Their revenues have grown historically at 3-4% other than COVID barely beating out inflation. Even the investor presentation seems to indicate that the market for injection based devices is expected to be flat over the coming 5 years.

No growth in the core business isn't the end of the world. I don't think your valuation really takes it into account but it does mean I'd like to see a very large margin of safety based on TTM performance.

My biggest worry is how their cashflows will actually be used. They seem to want to do bolt on acquisitions and research. Based on my reading the diabetes treatment business is competitive with all big pharma players involved to some degree. There are a large number of new treatments in development. I don't have a lot of confidence that if EMBC invests their cash flows in acquisitions and research it will provide a good ROE.

The patch pump is interesting and as you noted. There is a pure play in the space TNDM. Which gives you an idea of potential upside if they are successful. But it's hard to known if and when they'll actually be able to start selling their pumps.

It also worries me that CEO and CFO are both external hires from outside BDX. The overall board also owns almost no shares as you pointed out.

For now I think this is a stock I put on my back burner and keep reviewing to see if I can become more comfortable with the plan moving forward. Thanks again for the interesting article!

Interesting write up. The baseline valuation look good on the surface given the quality of the business. Along with the spin dynamics it's pretty interesting.

Wonder what you think about the managements plan for reinvestment? Are you worried about management wasting the businesses cashflows?

I'll have to dig in some more.