Quick Pitch: Red Cat Holdings (RCAT)

America's single, publicly listed small drone manufacturer capable of scaling is on the verge of a transformative contract win...

Original Post: 30/07/24

I came across this idea a few days ago. It was posted by Multibagger Monitor, and I wholeheartedly encourage you to read that more detailed write-up, with full credit going to that author. The reason I am posting here is to clarify my logic on the pitch and share the idea with readers. Though very clearly asymmetric in its outcomes, this idea is definitely speculative, and so it could make me look either very smart or sort of stupid. Regardless, we live and learn.

As brief context, Red Cat Holdings (RCAT) is an American micro-cap specialised in small defence drones with the ability to scale-up production. RCAT’s primary revenue contributor is Teal, which it acquired in Aug 21 for $10m. Teal was founded by the young inventor and Thiel fellow, George Matus, in 2015. Following a short and unsuccessful stint in the consumer market, Teal pivoted to making and selling small defence drones to government customers, specifically the US and NATO militaries.

With an undisclosed upgrade of the Teal 2 short-range reconnaissance drone, named the Teal 3, RCAT is now in a final duel with Skydio’s X10D for the award of the U.S. Army’s and Defense Innovation Unit’s Short-range Reconnaissance Tranche 2/3 (SRR T2) Program of Record. This scheme started with 37 competitors and calls for 12,000 small unmanned aerial systems (sUAS) to be sourced over a 10-year period. Users will be platoons of Army soldiers, allowing them to be aware of happenings in the next terrain.

Though there is minimal information on the numbers generally, each sUAS consists of two drones plus other equipment, and a unit could cost up to $65,000 versus $40,000 for T1, which Skydio was awarded in Feb 22 (Teal was still being integrated and had no fully prepared production facility). The T2/3 contract award is scheduled for Sep 24.

As conflicts in the Ukraine and Gaza have shown, drones are the next big battlefield innovation. And America’s drones, despite its obvious military supremacy, are surprisingly bad. The simple reason is that they have not been tested in combat. They remain expensive, hard to repair, fall victim to glitches, and struggle with electronic warfare conditions. Skydio, as the largest American small drone manufacturer, sent about one thousand drones to Ukraine, with poor results as acknowledged by its CEO.

“The general reputation for every class of U.S. drone in Ukraine is that they don’t work as well as other systems…”.

“[The Skydio X10 is] not a very successful platform on the front lines.”

Importantly, this failure extends to all American drones in Ukraine and not Skydio’s alone. The article was also written in Apr 24, and is therefore up-to-date.

As far as I know, Teal 2 drones have not been sent to Ukraine, so RCAT received all of the feedback at minimal reputational cost. Ukrainian troops have instead turned to Chinese DJI drones which, though commercially-oriented, make up for all the shortfalls mentioned above.

Meanwhile, the U.S. government has realised that it needs to put its own drone industry on steroids, and quickly. Besides the SRR T2 program, there is the Replicator Initiative, announced in Sep 23. $500m has been earmarked for Replicator in CY24, with a similar amount planned for CY25. The first tranche will include sUAS (RCAT’s category), unscrewed surface vehicles, and counter-UAS equipment. The high volume of this program is backed by Ukraine’s apparent consumption of >10,000 drones per month.

There are also more indirect factors that could benefit Teal. A DoD-wide ban on DJI drones was passed in 2020, and in 2021, DJI was placed on two sanctioned entities lists for national security reasons. The American Security Drone Act (ASDA) has also been introduced to legislative bodies. In brief, it would ban the purchase and use of drones produced in certain countries such as China and those under its political influence by federal departments and agencies, increase sourcing oversight, and also open the way for government funding and grants for domestic manufacturers. ASDA seems likely to pass.

On the consumer side, the Countering CCP Drones Act is in the works, which would effectively eliminate DJI’s drones from the consumer market, creating a huge vacuum that Skydio and RCAT both can and would like to fill (the two scale players; George Matus expressed a longer-term desire for Teal’s commercial entrance). Despite consumer pushback and the clear economic negative this would be overall, the U.S. government’s voice will likely ring loudest in what is an extreme form of protectionism.

The facts, then, are as follows.

Drones are increasingly critical to global forces.

Hence governments, at least those that depend on their military prowess as the U.S. does, are very likely to invest heavily into this space.

As with all military technology, on-shored production is preferred. The U.S. will, of course, never buy its defence drones from China, which is a real threat in the South-China Sea.

Skydio and Teal are the two U.S. firms capable of producing sUAS at scale, and hold all the relevant certifications e.g., Blue UAS.

In regard to RCAT, then, we are left with a simple question: what is the firm worth in a status quo scenario compared to an SRR T2 win scenario?

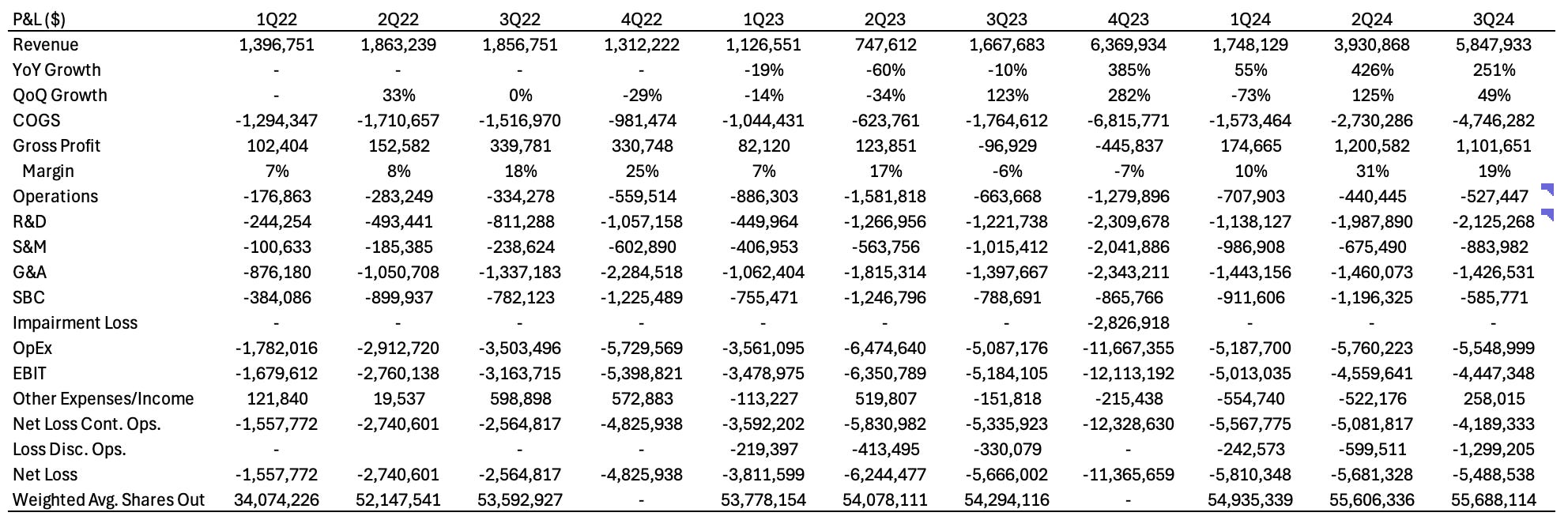

With low and unstable gross margins due to what are still suboptimal production volumes, a valuation based on EV/Sales seems most appropriate. Management has stated gross margins could hit 50% at mass production, which would be brought forward by a SRR T2 award. This seems appropriate, having found that AeroVironment’s average for its products is 40%. With its wholly-owned 25,000 sqft manufacturing facility in Salt Lake City, RCAT could make more than a thousand Teal 2/3 drones per month compared to current output of a few hundred.

Based on the below contract math, RCAT’s share price might conservatively hit $7.3 post- SRR T2 win. This is if we continue the current LTM 8x EV/Sales multiple on SRR T2 sales plus $28m annually, which is straight-lined revenue based on a 4Q23 $7m expectation. The 8x multiple is far less than AeroVironment’s 21x and Skydio’s 22x (private). This is because both benefit from economies of scale and are more established players generally, with several contract wins behind them (less risky contractors).

Excluding SRR T2, the share price would be $3.1 based on business-as-usual revenue of $28m alone.

Expected value, then, assuming a 50% probability of the contract being awarded, is $5.2, for a 127% upside.

Now for a short comparison of the drones contending for SRR T2. XD10 does perform well on paper specs. But I would agree that weightings are important, and there are numerous good reasons that Teal should win this contract. First, the Teal 3 has superior night-time technology: most missions, whether combat or border patrol, are flown at night. Second, unlike the XD10, Teal 3 is specifically constructed for the defence niche, which likely makes it a more rugged and reliable piece of equipment. Third, the Teal 3 is more interoperable and modular, from both a hardware and software angle, giving it a longer lifetime and flexibility. Importantly, this also reduces buyer lock-in and dependence, a common concern for government buyers.

Note that the specs below, besides the electronic warfare resistance, are those of the Teal 2. Assume those have been significantly upgraded.

Of course, Skydio still benefits from an incumbent advantage, which should certainly not be discounted.

Straight-lining last quarter’s sales and OpEx and using AeroVironment’s 40% gross margin, RCAT should break even at $13.9m in quarterly revenue. Pair this with the extremely high YoY growth rates in recent quarters as Teal 3 scales, and this target is definitely within reach.

Still, my primary concern is the cash burn, which I estimate at $5.1m per quarter based on the 9M23 statements and which puts a countdown on things. Yes, dilution is disincentivised through insider ownership of roughly 40%; the last capital raise took place in Dec 23 for 18.4m shares, producing a net inflow of $8.4m. But unless the anticipated 20% i.e., $78m upfront cash payment is received with the SRR T2 win (not $156m as I assume half and not all SRR T2 revenue goes to Teal), financing could be tight. RCAT also has no more marketable securities left, having fully exited its Unusual Machines stake for $4.4m in Jul 24, which again increases the potential for dilution.

“With military modernisation, the defence drone industry is in a rapid growth and innovation cycle […].”

“This sea change is driving robust demand for Red Cat’s Family of Systems both domestically and internationally. As a result, we’ve achieved three quarters of record revenue while reducing cash burn during the first three quarters of our year ended April 30, 2024, making this non-dilutive capital highly valuable for our strategic growth plans.”

- Jeff Thompson, RCAT CEO in Jul 24 Press Release

From a liquidity standpoint, RCAT’s management thinks it is good to go for the next year, citing the acceleration of business and scaling up of production. Its quick ratio stood at 3.6x as of 3Q24 with net cash of $6.8m.

As mandated and price-insensitive buyers, governments make for fantastic customers. And as to why this opportunity exists, the usual reasons are illiquidity ($1.8m average notional volume) and size. But there is also the complexity of this situation; I would have never found this thing on my own, and it would have taken a lot of time to figure out. Add to this ever-stronger ESG concerns and pre-Ukraine, next-big-thing fears similar to the weed industry: Matus explicitly mentioned that VC funding was hard to find for a prolonged stretch until Oman’s sovereign wealth fund stepped in.

I would normally pass on this type of speculative play, but the anticipated force of the U.S. government’s demand, protectionism, and obvious necessity of developing on-shored capabilities stopped me from doing so. In other words, there is too much asymmetry to ignore it.

Again, full credit to Multibagger Monitor for delivering on the original idea and providing deeper due diligence. There is also a second write-up by Cedar Grove CM, which claims to clarify some of the contract math, though the asymmetry still applies, even with those changes. I am putting this post out now because of its timeliness, and will update it once I know more.

Update: 01/08/24 CEO Call

Jeff Thompson was kind enough to clarify a few things in a short call today.

Teal 3 is the actual model in the run with Skydio’s XD10, and it has significant upgrades, most importantly electronic warfare (EW) resistance that Ukraine has highlighted as crucial; personnel there even refused to use free Teal 2 drones because they lacked this feature. Unsurprisingly, there is no publicly available specifications list for the Teal 3. Teal achieved EW resistance through its work with Doodle Labs, and we can assume its Teal 3 sports Doodle’s Helix Mesh Rider frequency-hopping radio. There is no other frequency-hopping radio out there that meets the stringent Blue UAS requirements within a single radio. Skydio’s XD10 has attempted a work around to fight EW through radio encryption, but struggles with this aspect of SRR T2.

In response to the potential of Replicator, Jeff mentioned that the Initiative is primarily focused on the threat of drone swarms in the Taiwan Strait (these are less of a thing in Ukraine). Through its exclusive collaboration with Sentient labs and weaponisation of its Edge 130 Blue product (contributed by Flightwave), which has the longest endurance of any comparable drone on the Blue UAS list, even AeroVironment’s, RCAT can effectively compete for allocations. Most importantly, the first go-to suppliers for Replicator selections are those established in Programs of Record. In other words, an SRR T2 win likely opens up lots of doors for RCAT.

Other points are that, generally, the math on the SRR T2 contract is in the right range, and that Program of Record announcements typically arrive in the mid-August to September range. This might bring forward the original inflection point by a few weeks. Cash burn reduction has also continued, and could make for a positive surprise come next week’s earnings.

Altogether, this builds more conviction in the thesis.

Disclaimer: this write-up describes the author’s own research and opinions. It does not constitute investment advice, whether explicit or implied. Invest at your own risk and do your own due diligence. I hold a material position in the issuer’s securities.

Yes, the US certainly does a good job of protecting and encouraging the development of parasitic loafers.

Just pointing out that your math is incorrect. You're right in stating that the $65k is per unit (2 drones) and that the contract is for 12,000 drones, but you mistakenly apply the $65k to 12,000 drones when it's actually 6,000 units (2 drones per unit).

That math alone brings down the contract from your $780M (similar to Mike's) to a more accurate $390M not including the extra parts, servicing, etc (flyaway costs).

You also can't apply VC muiltiples on public equities. $AVAV is more accurate and it's already on par with them

https://www.cedargrovecm.com/p/red-cat-rcat-trade-worth-up-to-200-prcnt