Market Mayhem (22/01/2022)

Market Mayhem (22/01/2022)

Peloton, MSFT-ATVI, and overall Anti-Risk

The Demise of Peloton

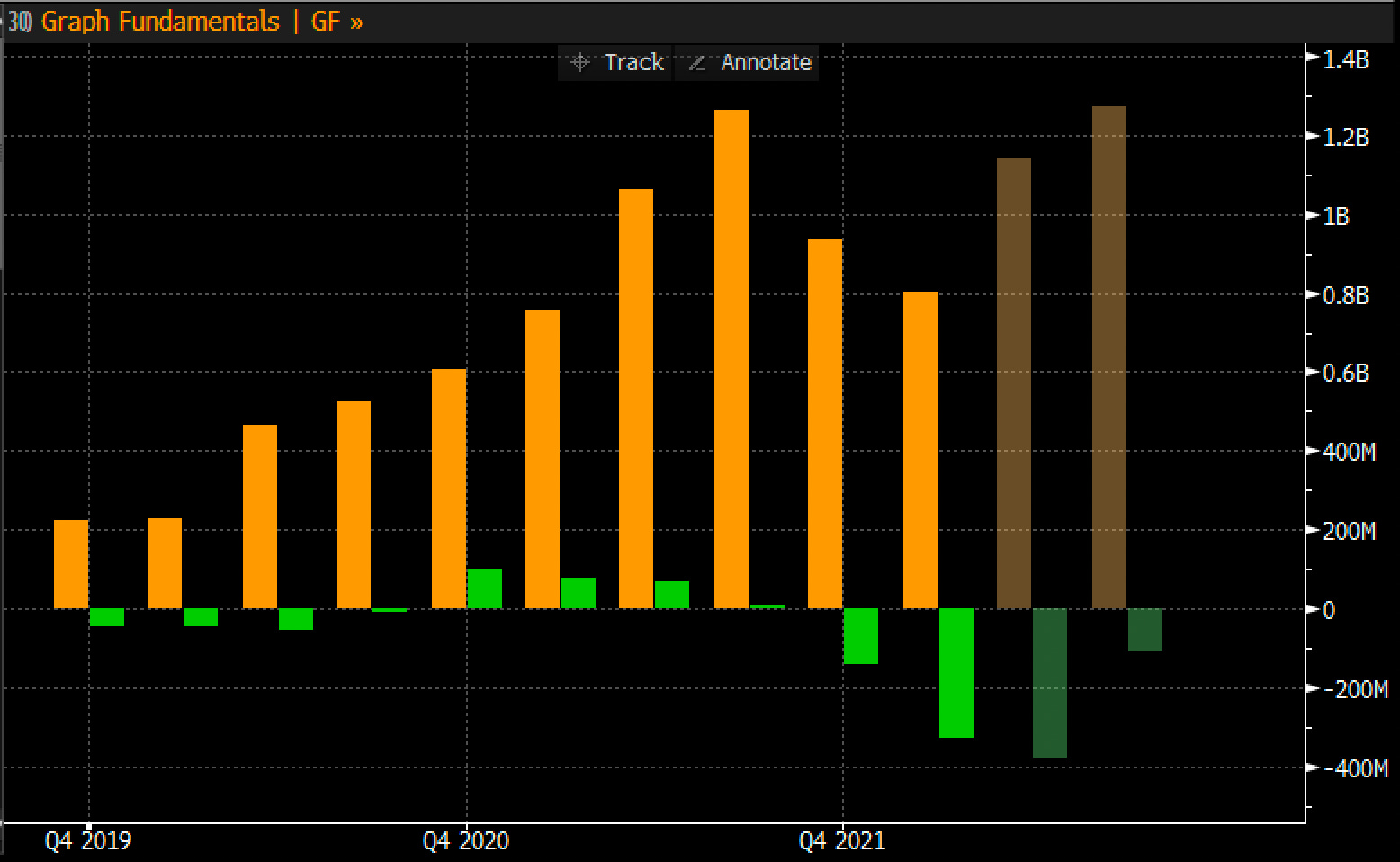

Peloton - the maker of connected fitness equipment - went public in September of 2019. The timing turned out to be excellent, as the introduction of lockdowns in Q1 of 2020 fuelled demand for the firm’s products. Indeed, between 2020-21, Peloton’s revenue doubled, from $915 million to $1,826 million.

It’s true that Peloton’s equipment is stylish and would’ve kept you fit in the face of gym closures - assuming actual use - but it’s also expensive. The basic bike costs $1,495 and access to the coveted online classes demands another $39 per month as a subscription fee. The offering is clearly premium, calling into question the company’s mission to truly ‘democratise fitness’. Doesn’t democratisation extend beyond white-collar, middle- and upper class families with plenty of disposable income on hand?

In a zero-interest environment where stocks appeared the only attractive investment and gyms were expected to be closed forever, it was perhaps inevitable that Peloton’s stock would attract speculators and shoot towards the moon at light speed (bless the golden gift of hindsight), and it did - for a while.

From an initial post-IPO valuation of $8 billion, Peloton rose to a peak of $49 billion in January, 2021. It all went downhill from there; Peloton has shed 85% of its market value in the past year, settling back at $7.9 billion, where it started. Insiders have also sold around $500 million worth of stock during that time.

The reasons for Peloton’s decline are interlinked. The firm rarely turns a profit, and whilst this is a typical feature of growth companies, investors do expect rapid sales growth. This expectation was met during the heyday of the pandemic, but no longer. In Q1 2021, the company reported sales of $756 million and operating income of $78 million. In contrast, in Q1 2022 (the latest), Peloton brought in $805 million in revenue (a marginal gain), paired with an operating loss of $330 million. The outlook is also poorer than before as gyms reopen and people get used to sweating in public again.

Moreover, the firm’s sluggish revenue growth is paired with declining gross margins in recent quarters. The bottom line: slowing sales and rising costs do not bode well for Peloton’s future.

If only management had a solution. At this point, they seem quite clueless. For example, in August of last year, management cut the costs of a peloton bike by about 20%, which drove a five-fold increase in sales within two weeks. Now, in a reversal, the price of a bike is being upped 17%, as Peloton shifts delivery and setup costs to its customers.

It’s not easy to simultaneously recover margins and reboot sales growth; raising prices would solve the former issue but exacerbate the latter, and vice-versa. Let’s not forget that people don’t need fancy exercise bikes like they need food or smartphones. Further, there are rumours that Peloton is embarking on a form of restructuring involving staff layoffs and cuts to production volume. To me, it seems that Peloton is the poster-child of speculative excess - time for a turnaround effort.

Blockbuster Deal

Last week, Take-Two Interactive scooped up Zynga. This week, Microsoft inked a deal to buy Activision Blizzard (ATVI) - maker of the Call of Duty franchise and World of Warcraft - for a whopping $75 billion in cold, hard cash.

The transaction is overshadowed by allegations of unequal gender pay and sexual harassment against ATVI, which now faces a lawsuit filed by the California Department of Fair Employment and Housing in July last year. To Microsoft’s pleasure, the event sent ATVI’s stock price down 30%, reducing its acquisition cost.

ATVI currently trades at $82 per share, but shareholders could receive $96 under the deal, suggesting that there is still skepticism as to whether the deal will go through. That’s understandable given the scale of the transaction; with ATVI in its portfolio, Microsoft’s video game revenue would jump by roughly half to ~$24 billion, and make it the third largest gaming firm, trailing only Sony Interactive and king-of-the-hill Tencent. In case you’ve been living under a rock, Microsoft is already a behemoth, with a market cap of $2.2 trillion and TTM revenues of $176 billion.

Microsoft’s main bet is on its Game Pass initiative, where players pay a monthly subscription fee for access to a library of games. Naturally, that library is now set to include ATVI’s well-known titles. 25 million gamers are already paying for the service, which replaces expensive, single title purchases.

ATVI’s CEO, Bobby Kotick, will exit the firm after the deal closes - with a handy $400 million worth of equity in his pocket. I’m sure that’ll make it hurt less. The acquisition is expected to close in July of 2023, subject to approval.

Anti-Risk

Investors, traders, and all others with portfolios continue to rush out of speculative growth and into value stocks, as potential rate hikes take their toll. Let’s look at some examples.

The Russel 1000 Value index has produced roughly double the return of the Russel 1000 Growth equivalent in the past year.

SPACS are the hipster’s method of taking a firm public. Here’s how it works. A blank-check company launches an IPO, promising to use the proceeds to acquire and merge with an attractive private firm. Post-merger, the private firm replaces the SPAC as the public company, now owned by the initial investors. If the concept sounds sketchy to you - it definitely is. Let’s shed a collective tear for those who took part in the gold-rush of SPACs, which tend to make insiders rich (they often receive options packages) but not investors. A certain SPAC index is down 34% in the past year, compared to a 14.5% gain for the S&P.

There’s blood in the streets for technology as well, with the MSCI World Information Technology index down 12% YTD relative to 6% for the MSCI World. Pot stocks are really another story (they burned), as nobody expected them to perform well anyway - right?

It seems that value and quality are in for substantial outperformance this year, but relative to what? The overall market or certain sectors? Here’s my prediction: the market will return somewhere between -50% to 20% this year. Prepare for the unexpected.