Market Mayhem (19/02/2022)

Market Mayhem (19/02/2022)

Buffett's ATVI Investment, Potential Russia-Ukraine Impact, and Netflix's Boeing Documentary

Buffett’s Activision-Blizzard Investment

The WSJ reported that Berkshire Hathaway invested in Activision Blizzard (ATVI) in October of 2021. In fact, 14.7 million shares were purchased at about $77, for a total value of $1.1 billion.

I immediately assumed that the timing would be impeccable - perhaps due to my blind faith in Buffett’s genius - but the investment was made before ATVI’s extended share price decline, and prior to the announcement of the Microsoft deal. That tells me that Microsoft must have scored quite the deal for ATVI - props to the CEO, Satya Nadella.

Berkshire’s investment is managed by Todd Combs and Ted Weschler, Buffett’s next-generation lieutenants. It seems this is another example of Buffett evolving his investment philosophy from a general skepticism towards technology firms - formerly outside his circle of competence - to recognition of their sometimes powerful business models.

Just look at the composition of Berkshire Hathaway’s portfolio. 48% of the firm’s capital rests in Apple. The stake has a total market value of $157 billion, and has produced an eye-watering profit of $32 billion. No other allocation even comes close to this level of significance. The ATVI stake is much smaller, representing only 2% of the portfolio.

Also, now that I look at this, Buffett is perhaps the most patriotic investor on the planet - all of his substantial allocations are to U.S. companies. For all the hype about his occasional overseas antics - like his investment in some Japanese trading houses last year - he does appear to be forever bullish on the U.S., first and foremost.

“When you next fly over Knoxville or Omaha, tip your hat to the Claytons, Haslams and Blumkins as well as to the army of successful entrepreneurs who populate every part of our country. These builders needed America’s framework for prosperity – a unique experiment when it was crafted in 1789 – to achieve their potential. In turn, America needed citizens like Jim C., Jim H., Mrs. B and Louie to accomplish the miracles our founding fathers sought.

Today, many people forge similar miracles throughout the world, creating a spread of prosperity that benefits all of humanity. In its brief 232 years of existence, however, there has been no incubator for unleashing human potential like America. Despite some severe interruptions, our country’s economic progress has been breathtaking.

Beyond that, we retain our constitutional aspiration of becoming “a more perfect union.” Progress on that front has been slow, uneven and often discouraging. We have, however, moved forward and will continue to do so.

Our unwavering conclusion: Never bet against America.”

- Warren Buffett, 2021 Berkshire Hathaway Shareholder Letter

Having laboured through a chapter or two of Ray Dalio’s book on the rise and fall of world powers - The Changing World Order - it seems clear to me that no nation remains king of the hill forever. But such a shift will certainly outlive Buffett, and perhaps myself.

What do you think?

The Potential Market Impact of a Ukrainian War

If you are like me, you might be growing tired of the constant ‘imminent invasion’ headlines, but they certainly seem to be influencing traders and investors. Thus, I thought it would be illuminating to explore the potential market impact of an invasion - after all, this is a finance blog.

Is the fear warranted?

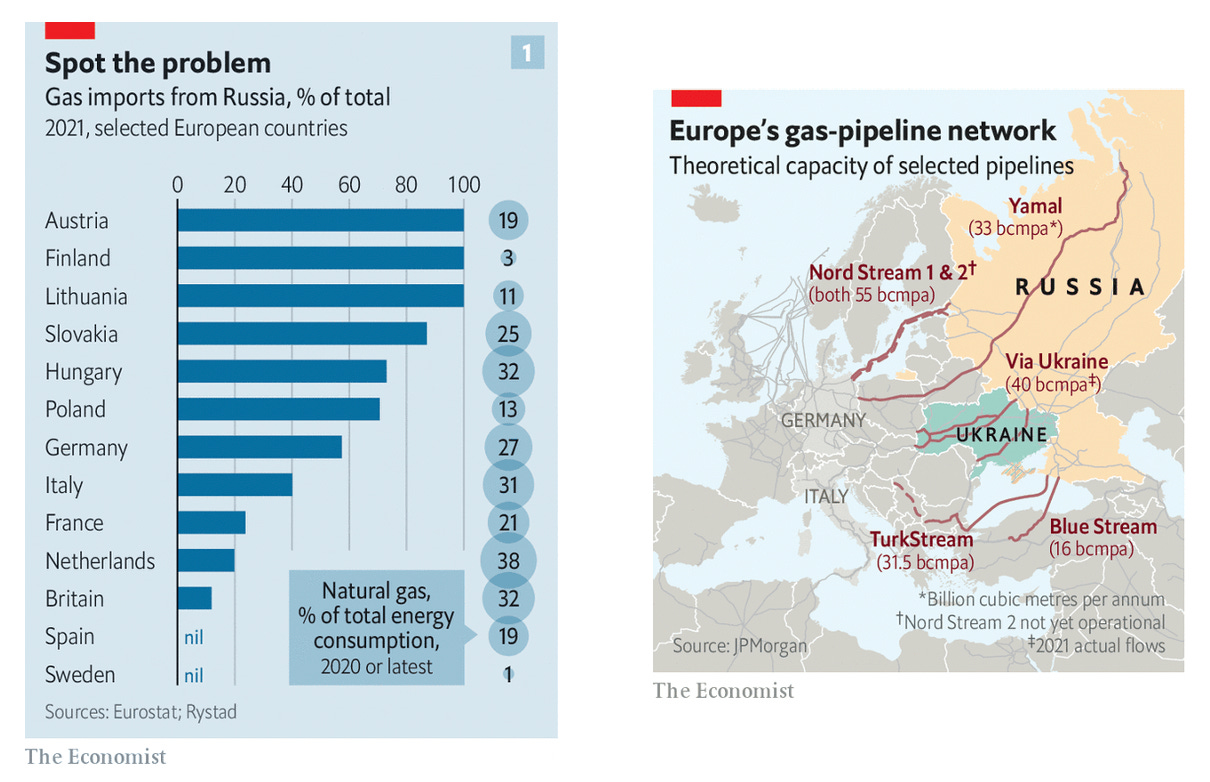

The West has repeatedly threatened to impose crippling sanctions on Russia should it launch an invasion. The problem is that sanctions cut both ways; if you punch somebody, you should expect to be punched back. That could have a global economic impact, and Russia punches above its weight class. Indeed, certain European countries are entirely dependent on its natural gas exports.

Besides gas, Russia holds third place when it comes to global oil production and accounts for about 14% of total mineral extraction (aluminium, nickel, palladium, gold, iron ore, etc.). That is all despite Russia having a smaller GDP than Italy ($1.5 versus $1.9 trillion).

It is also possible that an invasion could worsen inflation. To explain, if inflation is essentially more money chasing fewer goods, then cuts to supply would cause (is there really causality in economics) prices to rise. This would result in the usual price-hike spiral, which could accelerate countermeasures like central bank rate hikes.

If we view all of this from the traditional - and self-fulling prophecy -perspective, we might expect the following.

Safe-haven assets like gold appreciate.

Stocks depreciate, as businesses suffer from rising input costs due to inflation and associated expectations of accelerated rate hikes, plus reduced business, depending on the industry.

Predicting the effect on bonds is beyond me (I almost fell asleep trying to understand the link between rate increases and bond prices).

The prices of natural gas, oil, and certain minerals increase.

I have to be honest, I place no real value on predictions and instead follow the ‘stubborn mule’ doctrine: weather the storm and buy solid businesses on the cheap. It may be insightful, though, to look at a chart detailing market returns and periods of war.

Lo and behold, it seems investors simply shrug it off. Let us hope that Putin can be kept at the negotiating table.

Profits First, Safety Last: The 737 MAX

Netflix recently released an investigative documentary exploring the series of events leading up to and following the crash of two Boeing 737 MAX airplanes in late 2018 and early 2019. These incidents caused the deaths of hundreds of people.

In short, Boeing had been known for decades as a premier manufacturer of safe, well-designed airplanes. But following the merger with McDonnell Douglas, there was a marked change in culture, which led the firm to lose market share to its European rival, Airbus. Then, Airbus introduced the A320neo in 2010, which was extremely fuel-efficient (a key cost for airlines). In a bid to keep up, Boeing unveiled the 737 MAX.

New planes are often derived from prior models, and the selling point for the 737 MAX was that pilots did not have to be re-trained to fly it. But this was not actually true. Two planes in Indonesia and Ethiopia crashed shortly after take-off, and the recovery of their respective black boxes and other parts drove research that eventually revealed an uncomfortable truth.

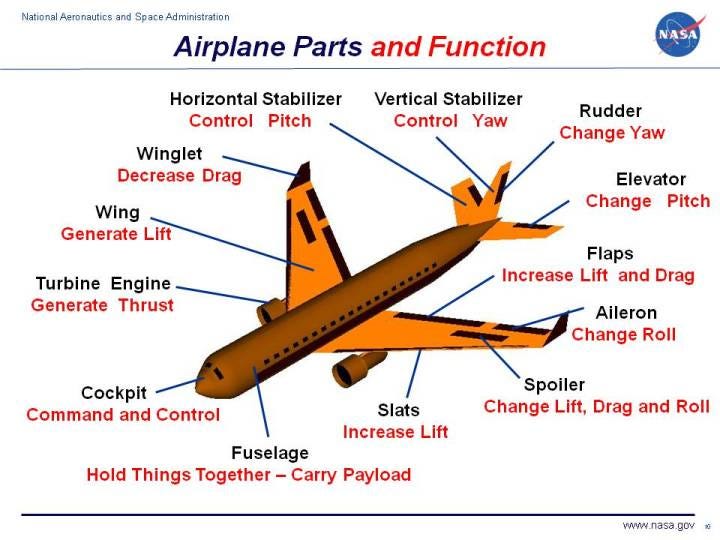

The 737 MAX had a new, so-called MCAS system added to it, which was intended to automatically correct the angle of attack by trimming the horizontal stabiliser (see image below, at the back of the model).

The issue was that the MCAS sometimes malfunctioned, forcing the airplane’s nose downwards and into the ground at more than 500 km/h. Even if pilots had been trained, they had only 10-seconds to initiate a manual override of the MCAS system before a potential catastrophe.

This was a textbook case of profit prioritisation, and management being corrupted by incentives. To make matters worse, the CEO - Dennis Muilenburg - eventually resigned with a $60 million package. The $2.5 billion dollar fine (settlement) issued to the firm later also shielded management from criminal prosecution.

The documentary is called: Downfall: The Case Against Boeing. I would highly recommend watching it!