Market Mayhem (15/01/2022)

Market Mayhem (15/01/2022)

Take-Two Acquisition, LG Energy IPO, and Beyond Meat

Take-Two Acquires Zynga

It’s been a splendid week for newer Zynga Inc. shareholders; on Monday, Take-Two interactive announced its intent to acquire the company for approximately $11 billion in cash and stock, as it seeks to expand its mobile gaming portfolio. Zynga’s industry is growing at a rapid pace, and the company has produced popular titles including FarmVille and WordsWithFriends. Take-Two launched the blockbuster title Grand Theft Auto back in 2013, with around 135 million copies sold.

Under the terms of the deal, Zynga Inc. shareholders will receive $9.86 for each share they own; $3.5 of that being cash and the remaining $6.36 Take-Two stock. The sum represents a 64% premium to Monday’s close of $6. Zynga’s current share price is $8.96, as the deal is not guaranteed to close.

According to Take-Two’s CEO, Strauss Zelnick, the combined firm will preside over 1 billion users - a massive cross-selling opportunity - with about 50% of net bookings (essentially revenue) coming from the mobile gaming space. Further, Zynga has its own marketing department, which is both rare and useful.

The offer also smells of opportunism. Zynga’s Q2 21 results suffered from a new policy introduced by Apple that required apps to ask for permission to track users. This made it difficult for firms to put out targeted ads and acquire new gamers; according to BranchMetrics Inc., less than 1/3 of individuals opt in to such a scheme. Zynga Inc.’s CEO, Frank Gibeau, described the changes as ‘profound’, although he also thought that most of the complications were behind the company.

Acquisitions in the mobile gaming space are flourishing. In 2021, Electronic Arts bought GluMobile Inc. for about $2.4 billion and Activision purchased the maker of Candy Crush - King Digital - for $6 billion in 2015.

South Korea’s Record IPO

LG Energy Solutions (LGES) is a top producer of electric vehicle batteries. The firm’s customers include Tesla, Hyundai Motors, and General Motors, and it plans to go public in South Korea, with an estimated raise of $9.2 to $10.8 billion, and an implied market cap of $59 billion.

42.5 million shares are being offered for about $216 to $252 a piece. The deal will set a record for the South Korean stock market, eclipsing Samsung Life Insurance’s $4.1 billion offering in 2010. Proceeds from LGES’s listing will be used to fund capex, reduce debt, and meet working capital needs.

The timing for the listing could be excellent, with investors’ appetite for the EV space appearing insatiable. This can be seen in the market performance of LGES’s Chinese rival, Contemporary Amperex Technology, since its listing in 2018. Indeed, the company’s share price has shot up from 25 CNY to 577 CNY in only three and a half years. That’s especially remarkable if we consider that overall Chinese market turbulence has generally sent investors packing.

The possibility still exists that the firm’s stock price performs well initially, and then tanks as appetite for speculative, growth areas of the market fades alongside rising rates, but maybe that’s just my skeptical value perspective. If the firm shows solid fundamentals - i.e., profitability - that will certainly put a floor under its market value.

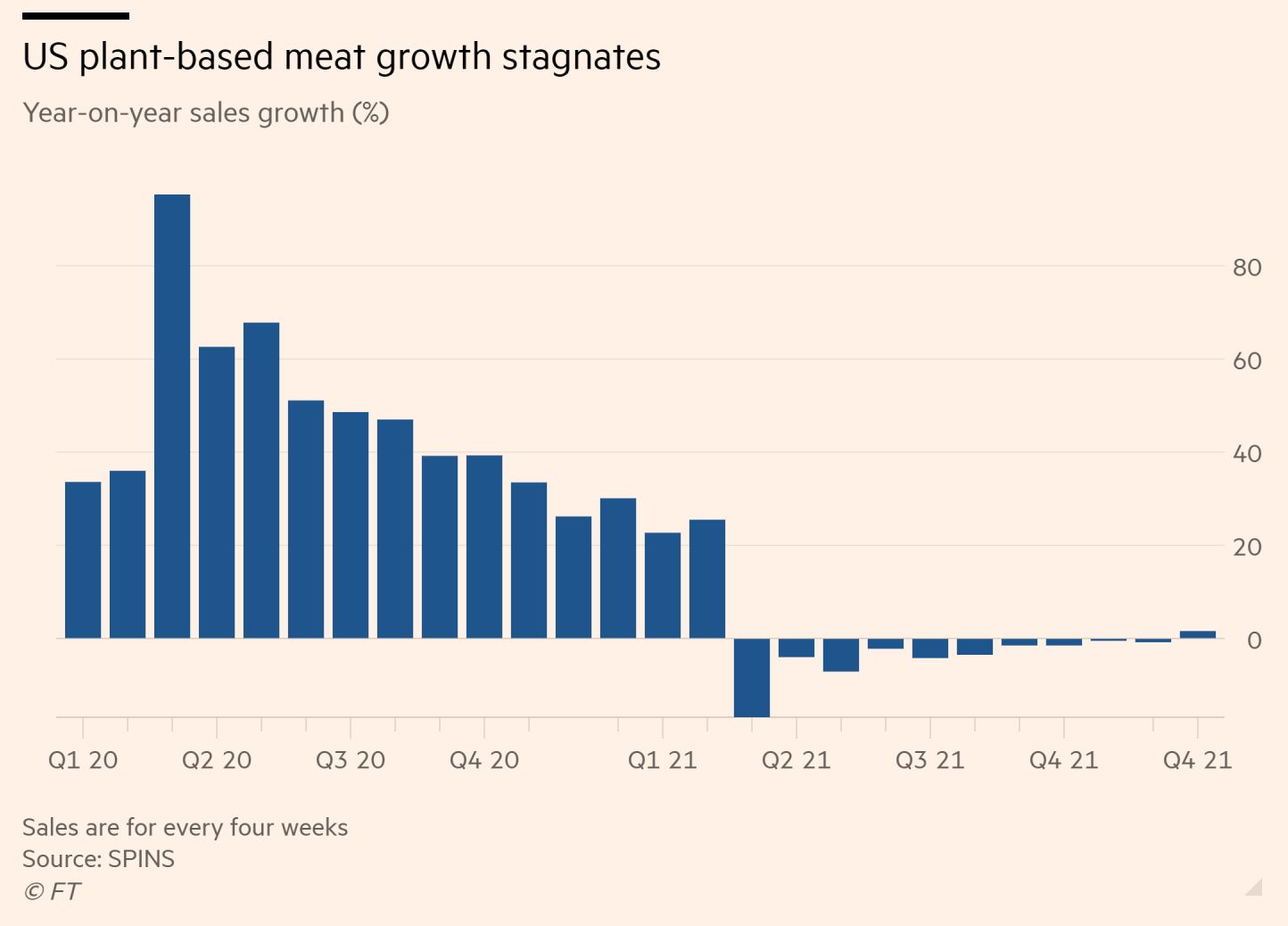

Beyond Meat on the Ropes

Investors - or should I say traders - are betting on the decline of the meat replacement firm Beyond Meat (BM), with 36% of the firm’s free float now being sold short. In other words, that’s about 20.1 million shares, up from 10 million in the summer of 2021, and the company only has 63 million shares outstanding. If short sellers wanted to cover their positions - which means repurchasing shares in the market to return them to lenders - it would take them nine days.

The question here is what the short thesis is. As the planet struggles to rein in climate change, plant-based meat should be an avenue through which wealthy individuals can make a change… right?

Well, plant-based meat consumption stagnated in the U.S. in 2021 - perhaps due to supply chain issues. It’s unclear whether this is a temporary or enduring phenomenon. Further, in October, BM warned that its Q3 21 revenue would fall short of expectations, and for Q4 21, the firm is guiding for an absurd range of $85 to $110 million in sales, representing a 17% drop or an 8% gain year-over-year.

Keep in mind that BM currently trades at a price-to-sales ratio of 9, which embodies expectations of serious sales growth. I’m going to stop short of saying the firm is overvalued - firms without earnings are a shot in the dark - but that does appear to be the consensus among short sellers.

In prior years, BM has succeeded in growing sales, but actual earnings remain out of sight for the foreseeable future.

Perhaps we will see another GameStop situation here in the form of a massive Reddit-driven short squeeze. I’m certain someone will be able to build a long thesis for BM sooner or later, especially with the launch of vegan nuggets in KFC branches and the Beyond Burger in McDonald’s. Investors have not reacted to this news with any enthusiasm.