Market Mayhem (06/03/22)

Market Mayhem (06/03/22)

The Russia Disconnection & Market Trends

Dear Readers,

You can’t fail to notice that almost everything else in the world of finance has been put on hold as the world digests the Russia-Ukraine crisis. I continue to hope for a diplomatic solution, and have deep respect for Ukrainian resistance. With that said, I hope you enjoy this week’s Market Mayhem.

Share your opinions in the comments section!

The Russia Disconnection

Surprise, surprise: Putin’s insatiable appetite for Ukrainian land will cost Russian citizens dearly. The sanctions levelled against Russia are the most severe in decades. In fact, analysts estimate that said measures will shrink Russia’s GDP by about 20% this quarter.

Several Russian banks have been disconnected from SWIFT i.e., the curiously named ‘Society for Worldwide Interbank Financial Telecommunication’. SWIFT essentially allows banks across the globe to send and receive transfer requests. There are alternative systems, but SWIFT is the most popular by far. Headquartered in Belgium, SWIFT connects around 11,000 financial institutions across more than 200 countries and is a member-owned cooperative (North Korea and Iran are excluded).

So, if the aim is to freeze money movement in and out of Russia, why disconnect only some - and not all - Russian banks? Just remember Europe’s Achilles heel. The continent is dependent on Russian energy, and that won’t change for a while yet. That’s why those Russian banks involved in oil and gas transactions were left untouched. Both Putin and European leaders know exactly where the pressure point is.

There’s also been a widespread corporate exodus. The payment behemoths, Mastercard and Visa, stopped processing foreign purchases for Russian citizens. Apple has stopped selling products in Russia and turned off its Apple Pay feature. Google also turned off smartphone-enabled payments and suspended all advertising.

In the oil and gas space, BP was forced to sell its 20% stake in the state-owned Russian oil producer Rosneft. Shell plans to exit all joint ventures with Gazprom, which is also state-owned. IKEA is shutting all of its stores in the country. Boeing and Airbus are withdrawing support to Russian customers and halting shipments of plane parts. Nordstream 2 has been put on hold, and the German operator of the pipeline is rumoured to be near-bankrupt. If all this seems intense, you should note that policies of this type are being mirrored by hundreds - if not thousands - of other firms too.

There are lots of other measures, but these are beyond the scope of this newsletter.

I should comment on the Russian central bank, which is under serious pressure. Faced with a plummeting Ruble, it doubled interest rates to 20% to attract foreign investment (best of luck with that) and domestic savings. Residents still want cash, and quick - ATMs are crowded.

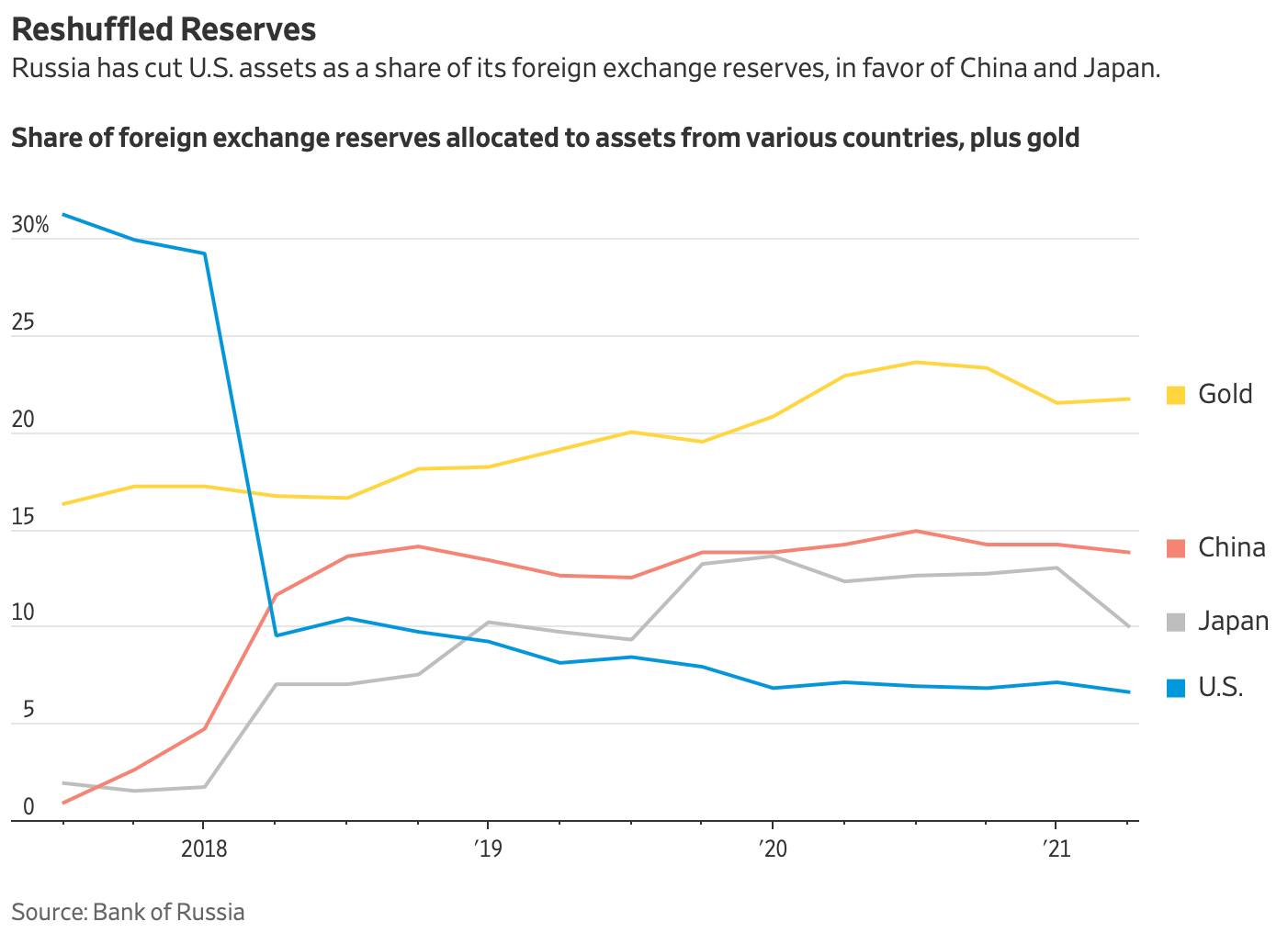

The bank also holds $630 billion in foreign reserves, which have now been compromised by Putin’s actions. 40% of the FX reserves are in countries that supported recent sanctions, and that’s despite Russia’s multi-year effort to shield itself from sanctions by reducing, above all, U.S. exposure (see the chart below).

Moody’s, Fitch, & S&P have slashed Russia’s credit ratings to junk, and the Moscow Stock Exchange has been shut for the entire week. The London-traded American Depositary Receipts of former titans like Gazprom, Rosneft, and Sberbank, have all declined more than 90% before trading suspensions, which doesn’t bode well for the MOEX’s potential reopening. For a while, investors could get exposure to Russia via ETFs, like the VanEck Russia instrument (RSX). But this fund has fallen from $25 to $5 and is now also suspended. Many will be liquidated.

Anyway, I’ve said it before and I’ll say it again: someone, somewhere, is going to make a fortune scooping up Russian shares at rock-bottom prices. This assumes that they will ever trade on a liquid market again. Some have mentioned the idea of nationalisation, which doesn’t seem too far-fetched anymore; Putin invaded Ukraine, and nobody thought he would. Whether he will succeed, though, is another question entirely.

Foreign asset managers, who had about $86 billion in exposure to Russian equities at the end of 2021, are now having serious trouble unloading their holdings. With no liquidity and a central bank instituted ban on brokers making sales of Russian assets on behalf of foreigners, they face massive write-downs. Finally, Powell will still seek a quarter-point rate increase this month.

So, we’re left with a unique cocktail of: record-low yields on bonds, runaway inflation, a war in Ukraine, the NFT and EV craze, rate hikes, and continued supply-demand imbalances. Talk about a setup for 2022.

Market Trends

The market climate has cooled off this year, and so has the value of equity deals. In February, about $24 billion worth of IPOs and additional offerings were announced, as compared to $170 billion in the prior year period.

Defense firms stand to benefit from the Russia-Ukraine war, as NATO’s requirement that members spend 2% of GDP will now appear necessary instead of prudent. I presume that much of the equipment will come from the U.S.

U.S. oil and gas firms should do well also, as Europe seeks alternative non-Russian suppliers and invests in its own energy infrastructure. Indeed, Germany, which is perhaps the most dependent on Putin’s resources, has already announced the construction of two LNG terminals.

The rotation from growth to value year-to-date also appears to persist. The Russell 1000 Value Index has lost only 3% in 2022 compared to 15% for its growth equivalent.

Finally, valuations have come down to earth. Now we’re at the end of Q1 22 and the S&P has an earnings multiple of 22x compared to about 30x in the prior year period.

The EUROSTOXX 600 index also trades at a pessimistic earnings multiple of 14x.

In a way, this is quite a relief - it suggests that the speculative fervour has begun to fade. Bring in the bargains!