Long Pitch: Kitwave Group (KITW)

Long Pitch: Kitwave Group (KITW)

The independents' independent wholesaler.

Investment Case

Powerful value proposition, appropriate strategy, and long runway.

Kitwave provides the highest-quality delivered service (almost perfectly on-time and in-full) at fair prices and with very low minimum order values (≥£100). These value propositions were once considered mutually exclusive, and their combination ensures that Kitwave offers an equivalent if not superior alternative to cash-and-carry giants and local delivered wholesale players. Moreover, Kitwave regularly acquires the latter i.e., its direct competitors, who approach management off-market due to Kitwave’s reputation as a “good owner” (no micro-management; “if it ain’t broke, don’t fix it” attitude). With a 5% market share and still very fragmented UK market, there is lots of potential to reap the rewards of this strategy long-term.

Real competitive advantage and attractive financials.

Through greater scale, Kitwave has more bargaining power over suppliers than its smaller competitors. Hence it can negotiate lower prices, the extra margin of which is reinvested into higher-quality service instead of undercutting competitors on price. This erodes the exact value proposition of said rivals, and this advantage is likely to widen over time. Larger-scale wholesalers/distributors have neither the appropriate infrastructure nor the desire to compete with Kitwave (would not “move the needle”). Moreover, in the past, Kitwave has grown revenues at a 13% CAGR, with industry-leading ROICs and margins, and cash generation is very strong.

Clear signs of a strong and prudent culture.

Paul Young founded Kitwave in 1987. From the start, he was focused on providing a high-quality delivered service to win against cash-and-carry stores’ lower pricing. Given his significant stake (still at 16%), Young never took a bonus, even though he could have, and his strategy of organic plus inorganic growth has been carried forward by Ben Maxted, who took over as CEO in Mar 24. Young effectively mentored Maxted, and it is a good sign that Maxted saw no need to overhaul the business purely to make his mark. Managements’ compensation is also very reasonable.

Business Description

Core Model

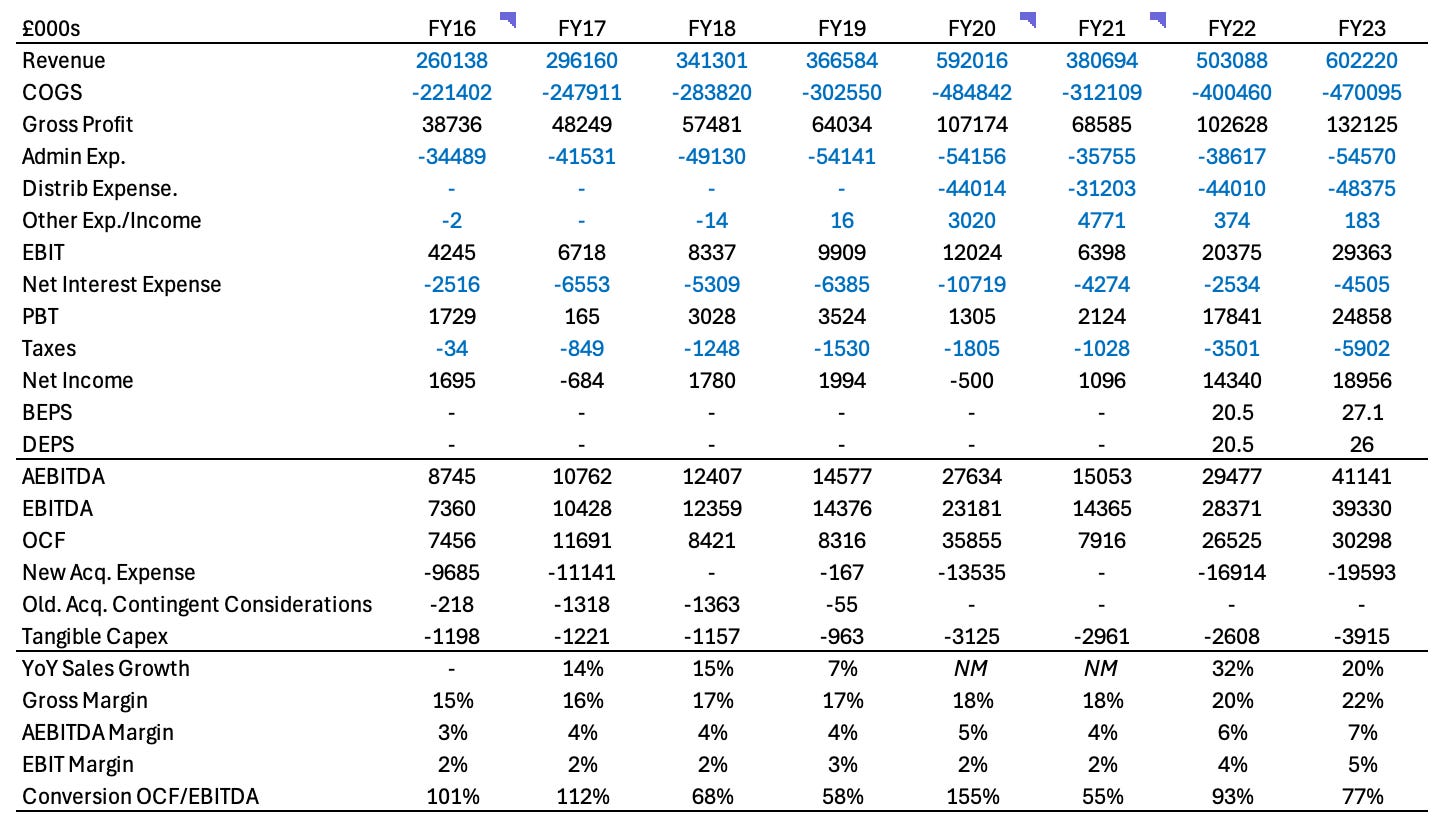

Kitwave, which listed on AIM in CY21, is a UK delivered wholesale business specialised in impulse products, frozen, chilled, and fresh foods, alcohol, and groceries. It supplies these products primarily to small, independent convenience stores and foodservice outlets, purely through delivery, and with an emphasis on the highest quality service. Kitwave’s assortment includes >44,000 SKUs sourced from >300 suppliers, and delivered to a national customer base of >42,000. Kitwave counts 32 depots across the UK, consisting of 10 main stock depots and 22 satellite depots.

Kitwave has grown both organically and inorganically (buy-and-build) from a revenue base of £260m in FY16 to £602m in FY23, a 13% CAGR, whilst increasing its gross margin from 15% to 22%, and its EBIT margin from 2% to 5%. The latter margin is double the average for Western European food wholesalers and distributors. Kitwave’s FY23 ROIC stood at 20%, with an average three-year OCF/EBITDA conversion of 75% and two- to three-week cash conversion cycle.

Kitwave’s model is the polar opposite of that which we associate with the biggest wholesalers (Booker, Brakes, etc.). Indeed, whilst the latter provide high-volume, high minimum order value (≥£1,000), and low frequency drops, Kitwave delivers low-volume, low minimum order value (≥£100), and high-frequency drops (>5,000 per day) to said independents within 24-hours. It does so through a fleet of 600 vehicles (equally split between leased and owned). Kitwave’s service levels are also excellent; in FY23, 98% of deliveries fulfilled the criteria of being complete and on-time. Overall, Kitwave ranks as the 15th-largest food wholesaler in the UK.

Segments

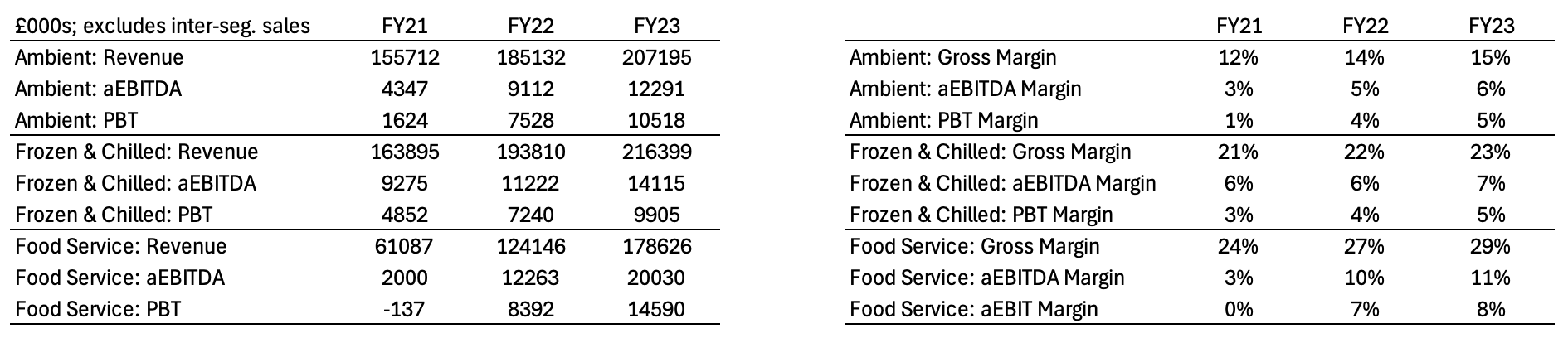

Kitwave’s reporting segments include Ambient, Frozen and Chilled, and Foodservice.

Ambient includes all foods and beverages that can be stored at room temperature. This segment accounted for 34% of FY23 sales and 30% of PBT, with a two-year CAGR of 15%. Customers include convenience stores, other wholesalers, vending machine operators, etc.. Margins in Ambient are lowest in the Group, partly due to discounted bulk sales to said wholesalers, tobacco sales, and the obvious lack of expertise required for this service because there is no spoilage risk. In this segment, Kitwave purchases through the Unitas buying group to benefit from collective bargaining power. It handles negotiations itself in the other two segments.

Frozen and Chilled accounted for 36% of FY23 sales and 28% of Group PBT, with a two-year CAGR equal to Ambient. Margins in this segment trend higher than Ambient because fresh and frozen products demand an uninterrupted cold chain. The main customers include chilled wholesalers, independent retailers, and cash-and-carry stores. Of course, there is a degree of seasonality here. For example, increased demand for ice cream in the summer means Kitwave typically leases a few extra vehicles for that period. Kitwave is a specialist in this segment, with even the largest distributor in the country, Booker (Tesco subsidiary), utilising its services under a special arrangement.

Foodservice contributed 30% of FY23 sales and 42% of PBT. This segment has grown fastest, at a 71% two-year CAGR, and its margins are far higher. This increased profitability is because the primary customers in this segment, specifically bars, clubs, restaurants, etc., have a far higher frequency of restocking (at least once per day), plus greater expectations in terms of quality, and higher opportunity costs. Given the attractiveness of this segment, it is not surprising that growth in the Foodservice segment is a strategic priority for management (see Acquisitions and Strategy).

A brief discussion of value propositions and the wider dynamics in Kitwave’s market is definitely valuable. Since convenience stores and foodservice outlets account for >40% and >20% of Kitwave’s revenues, respectively, the focus will be on these two groups.

The Perspective of Convenience Stores

Operators of convenience stores have limited square footage, and therefore focus on selling the highest-margin impulse products, like alcohol, vapes, snacks, soft drinks, etc. They typically restock three times per week, and can do so either through cash-and-carry stores (CaC; Booker, Costco, Bestway, etc.) or delivered wholesale. It is common for an operator to select one of its (on average five) wholesale sources as the “broadliner”, from which half of its SKUs are sourced. These relationships are sticky, and can last for decades.

18% of UK operators restock most products through CaCs, likely because they offer lower prices and might also have a sufficient selection of SKUs. This means travelling to the store itself, paying cash upfront, and transporting the products back to their shop for shelving. CaCs are more popular for the less successful operators, who also have a lower opportunity cost.

About 55% of operators utilise delivered wholesale for most of their SKUs. Here, their focus is on five sources of value: delivery of products on-time and in full, selection and consistency of SKUs, speed and frequency of delivery, minimum order values, and price. The sum of these factors decides service quality. Unlike CaC, delivered solutions offer credit to buyers and have no opportunity cost (47% of orders in Oct 23 were through Kitwave’s website), and operators might also receive value-added services, like range, marketing, and stock level advice. Moreover, for frozen and chilled products, specialised delivered wholesalers eliminate the risk of spoilage (convenience stores typically have very limited refrigerated space). It would seem, then, that delivered wholesale is the universally superior option for the average convenience store.

An important general dynamic in this space is that of symbol groups, which span 44% of independent stores. These groups, examples of which are SPAR, Nisa, and Londis, are not unlike franchise models. Members of said groups win the right to use the group’s symbol with its associated brand power and upgrades like point-of-sale systems and other assistance. However, in exchange, the store operators typically agree to make minimum purchase orders from their symbol group and linked distribution networks of, for example, ≥£1,000 in SKUs per week in the form of low-frequency drops. It is common for half of a convenience store’s budget to go to such a symbol group, though operators retain the right to allocate the rest of their wallet to another distributor, in particular for high-frequency, chilled and frozen products that a symbol group’s network is likely unsuitable for.

The Perspective of Foodservice Outlets

Managers of foodservice outlets like restaurants, clubs, pubs, etc., have an even greater demand for delivered solutions; >80% choose delivered. This is because they require a far higher proportion of perishable products, which means a higher restocking frequency; they also have a higher opportunity cost, as meals are comprised of several ingredients, so the lack of one ingredient means the whole ticket cannot be realised; staff have less bandwidth generally, having to actively tend to customers; and wider margins make the delivered premium manageable. Foodservice relationships tend be very sticky due to the higher switching costs, and symbol groups do not extend to restaurants because the latter have their own independent brands.

“Once you've got that [Foodservice] customer, if your service is good, they are very sticky and the price becomes slightly more inelastic in that vein in terms of the ability to lose a customer on price.”

- David Brind, CFO, Kitwave Group

Other Customers

Vending machine operators (Selecta, Montagu, etc.), other wholesalers, and larger retail and discount chains make up the tail end of Kitwave’s customers. Deliveries to vending operators include snacks, soft drinks, cups, stirrers, etc., and these are sent not to the location of the machines, but to the customer’s depots.

Revenue from other wholesalers make sense if one considers that Kitwave can likely source products at a lower price through increased scale, and that manufacturers have actively raised minimum order values in the past half decade to force consolidation.

The largest customer in FY23 accounted for 7% of sales, and is likely an international chain, such as B&M European Value Retail or Domino’s Pizza Group. Kitwave supplies Coca-Cola and Ben & Jerry’s to DPG nationwide, and was actively selected by these firms instead of tendering. This highlights an opportunistic attitude towards bigger partnerships, with no intent to replicate the networks of the big wholesalers.

“We'll only look at those opportunities [larger chain partnerships] as and when we can do it on a wholesale basis and make a wholesale margin. We get approached for tenders for contract work. It's not what we're interested in. So it'll only ever be few and far between. Our reason for being is the independents. These make nice bolt-ons when we can make proper margins on them. And yes, they come with some nice bigger volume. £20 million at a time revenues. But it's only for the right and proper time. It's not something we actively chase. It's more when people approach us.”

- David Brind, CFO, Kitwave Group

Acquisition Track Record

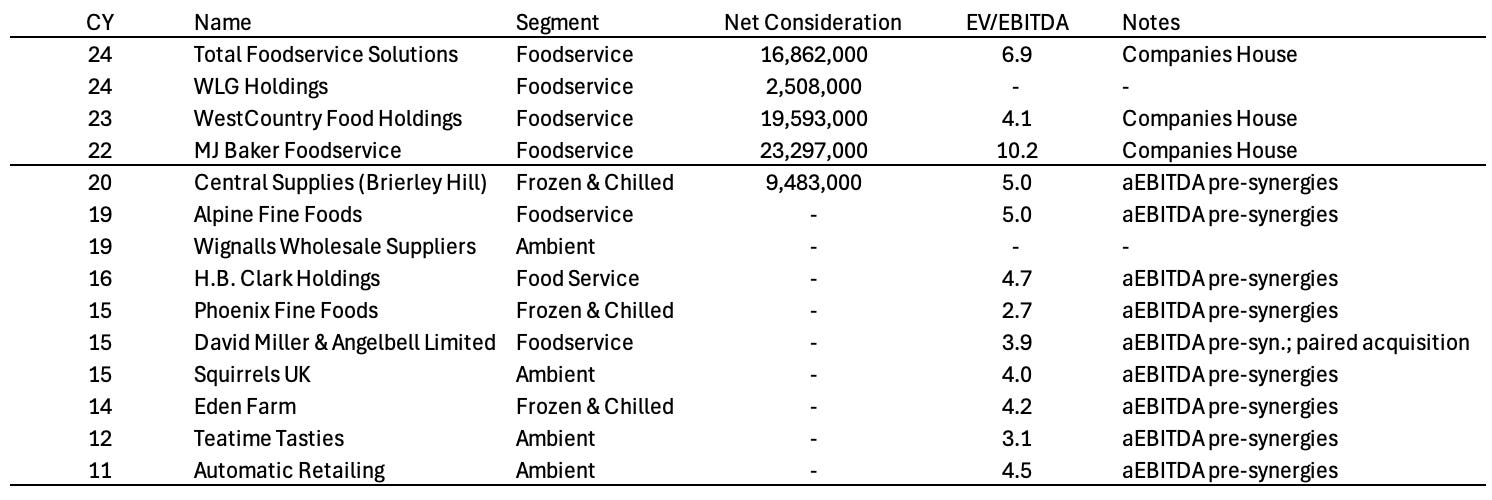

Kitwave has successfully completed 14 acquisitions since CY11. Management has three criteria for targets: family-owned and profitably run; widens either geographic reach, the customer base, or the product pipeline; can be acquired at an attractive valuation, specifically ≤5x pre-IFRS 16 and pre-synergies aEBITDA; is earnings accretive from the start; and does not require a turnaround, with potential for synergies.

Post-integration synergies can account for half if not a full turn of EBITDA according to management, and could stem from cross-selling, more bargaining power, fleet, depot, and route optimisations, and elimination of duplicative overhead.

It is difficult to determine whether this important EV/EBITDA criterion has been met in historical transactions because of the specific modifications to earnings and meagre disclosures by management. This can be seen in the difference between multiple estimates based on Companies House for recent transactions and the firm’s own EBITDA calculation as disclosed in its IPO prospectus.

Kitwave is an opportunistic acquirer, and is often approached by sellers off-market because they are seen as a good owner. Corporate takes a hands-off approach to acquired firms, changing nothing culturally, seeing as targets are often experts at what they do. Payments are primarily in cash, which is a welcome change from the accounting game of contingent considerations.

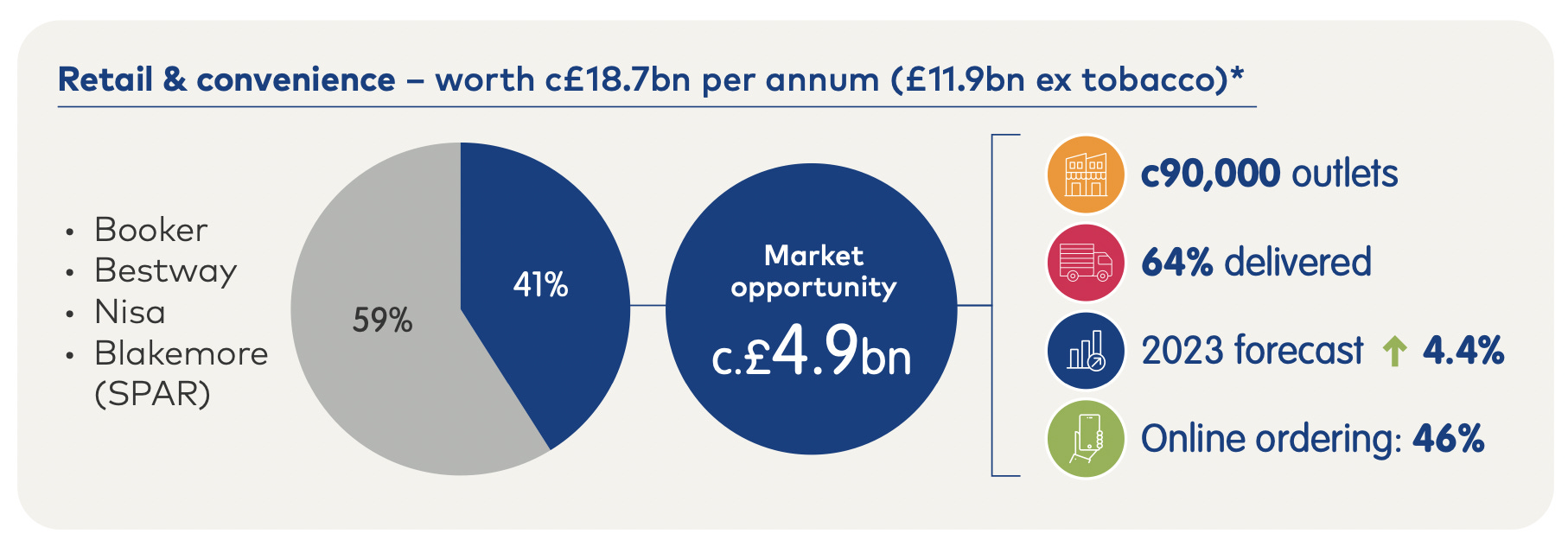

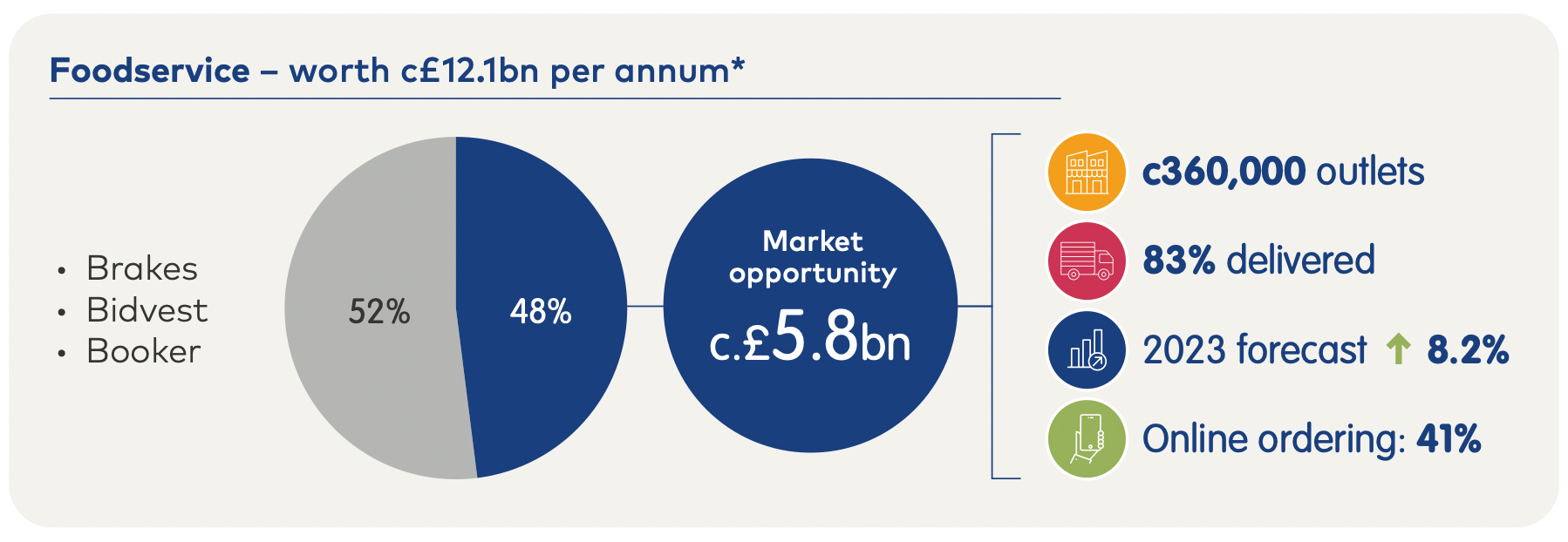

Market and Competitors

Kitwave separates its addressable markets into retail and convenience, and foodservice. In both, it excludes symbol groups like Blakemore/SPAR and other large-scale distributors i.e., it assumes their market shares are locked up/inaccessible.

This results in a SAM of almost £11bn, and a current share of 5%, so there is a long runway. What is not shown in the below screenshots is that this market is also extremely fragmented, with dozens if not hundreds of small-scale players.

In fact, Kitwave competes primarily with small, single-site local specialists, who provide excellent service within a radius of about 50 miles from their depot; it is no coincidence that these firms are also those Kitwave seeks to acquire. There is also some competition from smaller symbol groups in the convenience store space.

The defensive nature of Kitwave’s market is also notable. Total sales for convenience stores grew right through COVID, and restaurants saw a dip that was quickly recovered. In a more generic recession that is not pandemic related, we should expect a less severe downturn in restaurant demand.

“Restaurants and c-stores are two areas that capital will be going into for a long time. If you are Lamb Weston selling french fries to McDonald’s, you can be sure there will be more McDonald’s stores and that you will sell more volume over time. With restaurants, you will be certain there will be more restaurants the next year. On the other hand, you have to be careful with grocery stores. There is only so much capacity, and in some years the category just doesn’t grow that much. C- stores and restaurants are better than grocery stores and I haven’t seen any of them internalise their own distribution.”

- Board Member, Food Distributor

Competitive Advantage

Versus Smaller Players

The gut response here is scale, since Kitwave competes with local and regional players, who typically have revenues in the millions or tens of millions. But if scale effects tend to be local, how exactly does this advantage manifest?

First, we need to understand that a distributor does not need to work miracles to produce a reasonable return on capital. In fact, a single distribution centre combined with an acceptable SKU selection, a fleet, reliable workers, and a sharp operator is often sufficient to have customers stick around. With humble ambitions, a distributor might even have the pie to itself (a reason this market is so fragmented).

However, unlike the biggest wholesale players, which have no hope of delivering the same service level of locals at a similar price, Kitwave can deliver on both of these value propositions. With its national scale, Kitwave has more bargaining power over suppliers, enabling it to source products at prices that are up to 2% lower thanks to rebates, with the extra margin (double the Western European wholesaler average) reinvested into higher-quality service e.g., faster deliveries, lower minimum value orders, etc. This directly erodes what local players likely claim as their USP, and it forces them to make a painful choice: that of lowering prices or improving service. The latter seems more digestible, but Kitwave has absolute best-in-class service levels of >98% (management stated the industry average is in the low 90s).

Kitwave also has a far broader SKU range. This makes it a one-stop-shop with greater route densities, permitting lower minimum order values, which make for a fantastic value proposition when combined with “day one for day two” service.

“[…] the U.K. market is on “day one for day three” because “day one for day two” has huge premiums associated with it. So, if [Kitwave is] doing £75 minimum order day one day two within 25 miles, then that's a very premium service offering for a relatively small minimum order value.”

- Former Exec at Compass UK & Ireland

One should also not forget that distributor scale and service matters to the manufacturers at the start of the value chain. Logically, they would rather work with fewer distributors who can buy and handle more of their products to reduce their administrative burden, and they also want to protect their brand image through good custodianship. It is not uncommon for manufacturers to replace distributors when they fail on these demands.

As mentioned earlier, there is also a recent trend of cutting out smaller distributors through higher minimum order values to force consolidation in the industry. Diageo is one example (Gordon’s, Guinness, Smirnoff, etc.).

Last but not least, Kitwave provides unique ancillary services like range and stock level advice, the aforementioned electronic order platform (usage might cap at 60% as there is some generational reluctance), and live knowledge of products from manufacturers through its direct relationships with them. These might be provided in part by competitors - if at all.

Versus the Biggest Players

Most importantly though, why do the largest players not compete with Kitwave?

The short answer is that they are focused on big ticket, high volume relationships with national chains that have a food and beverage component, whether those be hotels, fitness providers, restaurants, etc. This focus demands a tailored infrastructure that, by default, eliminates the option of providing equally high service levels to small customers (it is either or).

For example, where Booker, Bestway, etc., utilise 44- and 26-tonne vehicles to make drops, Kitwave uses 12-tonne and 7.5-tonne trucks. Of course, the latter can navigate far denser routes. Kitwave also has smaller but more numerous depots on average, and might do multiple deliveries per day, whereas the largest players do perhaps four deliveries a week at the high end. Symbol group contracts also specify minimum order values of thousands of pounds, perhaps over years, which serves as further evidence of an infrastructure mismatch. It makes zero economical sense for the big boys to move the needle through targeting Kitwave’s independent customers; the assets are mutually exclusive.

Growth Drivers

Acquisitions are Kitwave’s inorganic growth driver, and management has guided for roughly two acquisitions per year.

On the organic side, volume is driven by increased cross-selling as the SKU selection expands (margin accretive, as Kitwave is making fixed cost drops regardless), net customer wins as the value proposition beats smaller players, general industry growth (market estimates point to low to mid- single digits), and significant post-acquisition synergies (overhead eliminations, asset rationalisations that make up PPE disposals, etc.). Historic organic revenue growth has been estimated at 3-4% by management, and price increases consist of inflation being passed onto customers (consumer staples benefit).

It is worth noting that continued acquisitions and expansion in the Foodservice segment is also margin accretive.

Management, Incentives, and Ownership

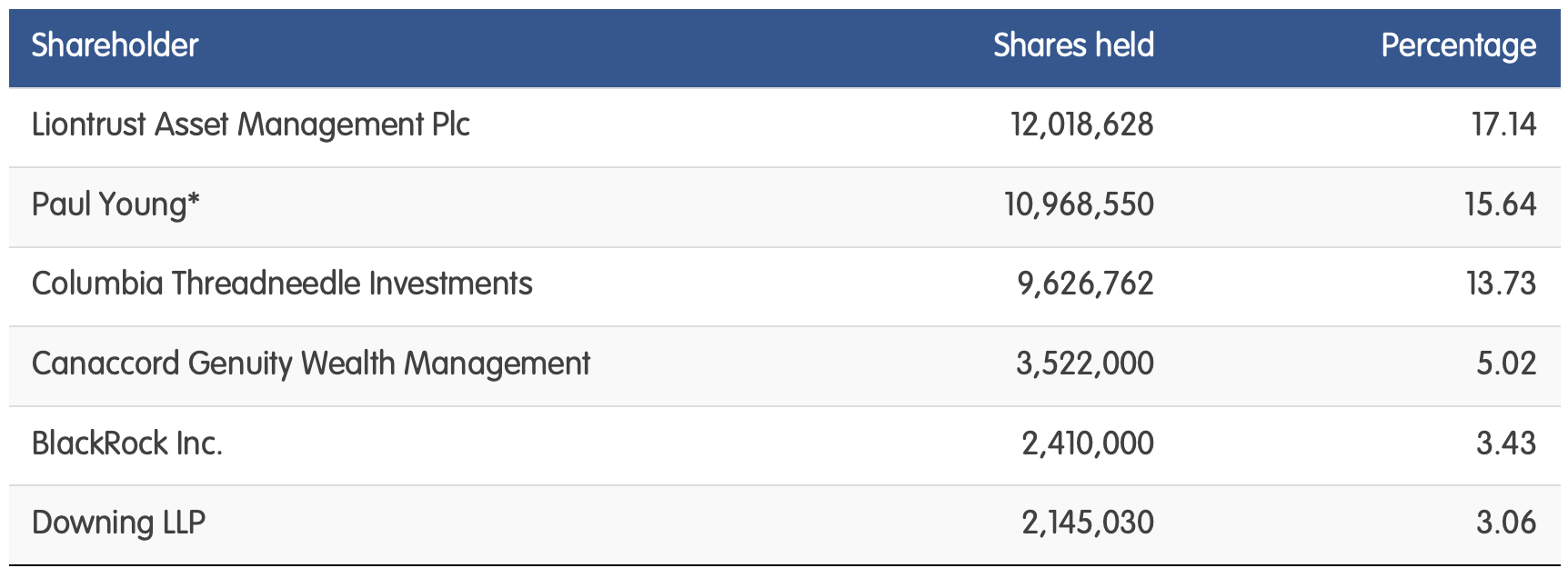

Kitwave was founded by Paul Young in 1987. Young retired in Nov 23, but together with his sons, retains about 16% of shares outstanding and looks forward to being a long-term shareholder. He has no intention to sell. Young was replaced by Ben Maxted in Mar 24, post-AGM.

Maxted has taken the approach of continuing Young’s perfectly valid strategy of organic and inorganic growth, which is a good sign. Maxted will be paid £410k base, with an annual bonus up to 25% of this based on outperformance of the market (Paul Young, in his former role of CEO, refused a bonus due to his stake in the business, which could be testament to a good culture, and he mentored Maxted). A LTIP was granted in Mar 23, vesting in Mar 26, worth up to 100% of base, and with a required two-year holding period post-vesting for executives. Metrics for the LTIP are based on fundamentals like EPS and total shareholder return.

The fee for the Chairman, Stephen Smith, is £95k, with £50k for non-executive directors.

As of FY23, Maxted held 70,456 shares directly, and 1,216,667 through options, worth £4.1m at the current price. David Brind, CFO, held 1,040,233 shares directly, and another 750,000 conditionals, for a total market value of £5.8m. The Chairman held about £161k worth of shares directly. Though the remuneration committee has not gone with the best long-term fundamental performance metrics, the size of managers’ interests suggests strong alignment with shareholders.

Besides Paul Young, other shareholders include various institutional small-cap funds.

Reasons for Undervaluation

Five reasons come to mind for Kitwave’s undervaluation.

First, the IPO in CY21 (midst of COVID) was not accompanied by a lot of fanfare and excitement; this is a very boring business. Second, there is one equity analyst covering Kitwave today, and he has consistently underestimated its performance. Third, there is a good deal of confusion in the historical reporting periods, and investors dislike short track records (3-years of uniform statements). Fourth, investors have a general distaste for roll-ups, and are often uncertain about whether value is being created. Fifth, though Kitwave has a simple model, it is not obvious where the competitive advantage lies/how Kitwave’s model is unique: Kitwave’s IR has not done a lot of the work for investors.

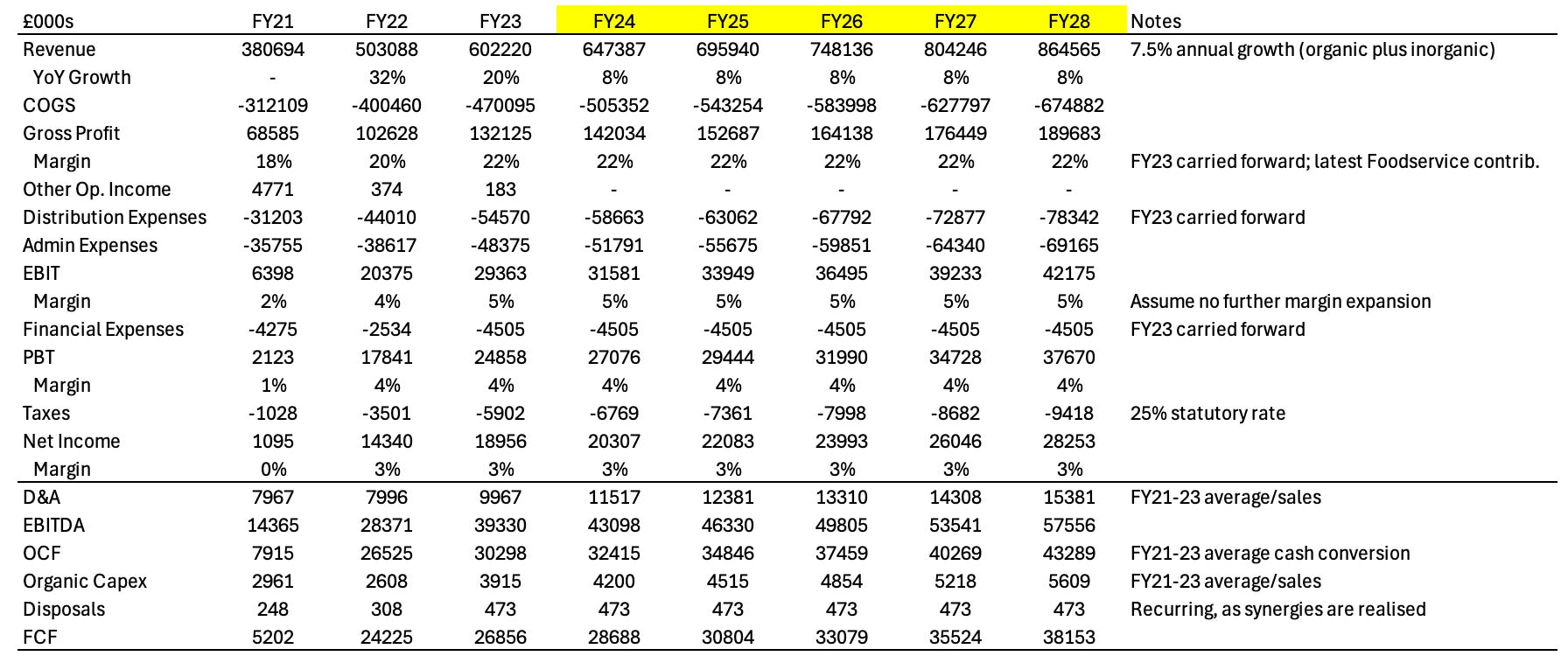

Valuation

Kitwave is difficult to value primarily because of its roll-up strategy. Specifically, the awkwardness stems from the fact that acquisition capex is part but also not part of core operations, such that an organic valuation excluding this recurring capex would print theoretical free cash flows that would likely be backloaded until acquisitions stop (whenever that might be), and are therefore worth less today. This is not to say that said acquisitions eliminate free cash flow, but they do eat up a significant chunk.

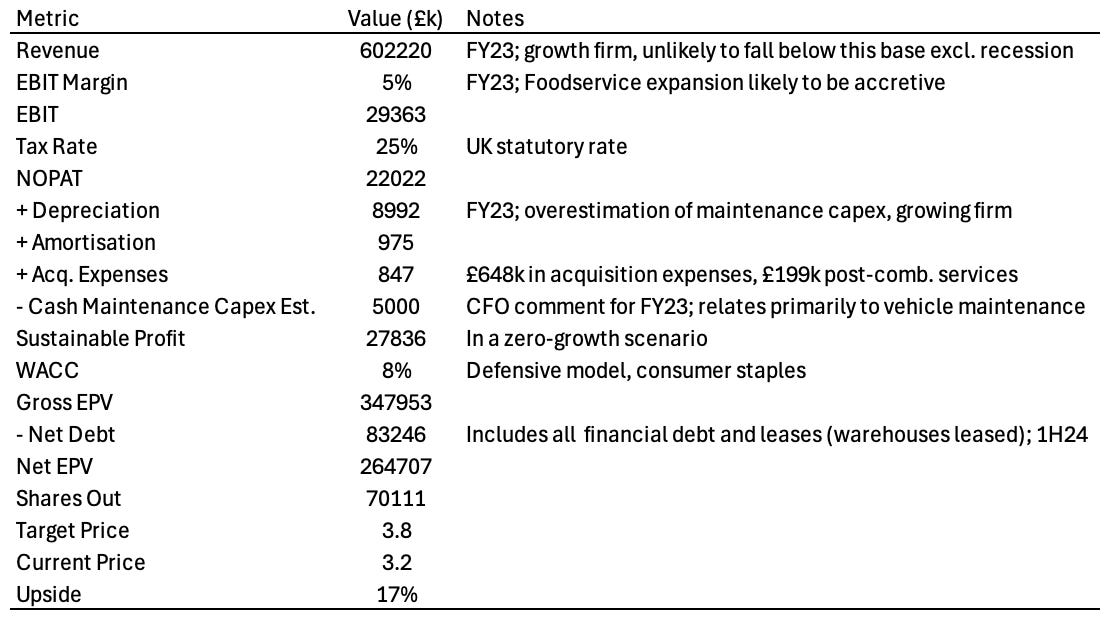

On an estimate of sustainable earnings power excluding growth, Kitwave might be worth about £3.8, a mere 17% above the current price. This suggests the market is not pricing in growth, which is odd considering Kitwave has grown at an excellent 13% CAGR since FY16, with no convincing reason as to why this should no longer continue (though pace is another question).

In a careful and conservative growth case, where I assume 7.5% revenue growth, zero margin expansion (despite potential Foodservice growth), a 25% tax rate, various historical averages for factors like depreciation and amortisation and cash conversion, and an 8x EBITDA exit in FY28 (the current multiple), Kitwave could appreciate 60% to £5.2 per share. The LFY earnings yield stands at 8%.

Though I am reluctant to bet on multiple expansion, it is definitely worth noting that peers, who are generally financially less attractive than Kitwave, trade at higher average multiples. With its strong and stable cash generation, Kitwave is also an attractive acquisition for PE or a bigger corporate.

Considering this valuation, and the defensiveness of the model, I believe Kitwave has a very limited downside, with the potential to compound strongly in the next decade or two.

This write-up draws on scuttlebutt and quotes from a more detailed piece written up by Sohra Peak Capital Management, available here. Kudos.

Disclaimer: this write-up describes the author’s own research and opinions. It does not constitute investment advice, whether explicit or implied. Invest at your own risk and do your own due diligence. I do have a position in the issuer’s securities.

Interesting write-up