Dr. Martens (DOCS)

A strong UK single-brand business, 8x oversubscribed at IPO, now left-for-dead.

Dear Investors,

I believe the UK is serving up some serious bargains right now. From a value perspective, it almost feels like shooting fish in a barrel… as long as one can ignore the deep uncertainty and macro angst, and hold for the long-term. First there was Moonpig PLC, and now there is Dr. Martens PLC. Both had recent IPOs under better conditions (the FTSE 250 is down 21% YTD) and have seen big selloffs. To no-one’s surprise, the worst performing sectors in the S&P 500 as of 12/12/2022 are communication services (-38%), consumer discretionary (-33%, Moonpig & Dr. Martens), and information technology (-24%). I filter for these exact sectors with a preference for Europe, as the poorer macro outlook has caused a greater discount and worse sentiment than in the U.S.

The business.

Dr. Martens’ origins date back to 1945, when former German soldier and doctor, Klaus Maertens, invented the air-cushioned sole to provide relief from the pain of his broken foot. Dr. Maertens sought to profit, and began a business partnership with Dr. Herbert Funk, selling their shoes primarily to older women (very successfully). In 1959, an overseas advert placed in a trade magazine was seen by the Griggs family, which was then a dominant producer of work shoes in the UK (the R. Griggs Group).

Impressed by the concept, the Griggs family decided to acquire exclusive rights to manufacture the sole and shoe in the UK. The first model, with a new design, was finalized in April of 1960: it featured the iconic black and yellow color scheme, a new sole layout, a simple, 8-holed upper section, and was named the 1460. Despite humble beginnings as a £2 work boot for the proletariat, the 1460 graduated to become an icon in certain youth subcultures and saw continuous, rapid sales growth throughout past decades.

The once-small Griggs Group sold its Dr. Martens PLC subsidiary to Permira PE in 2014 for £300m. Following a comprehensive transformation and professionalization, Dr. Martens was taken public through an IPO on the LSE in Jan 2021 with an offer of 402.5m shares at 370p (including a 52.5m share Greenshoe option). The deal was 8x oversubscribed and priced at the top of its range. Permira, the principal shareholder, sold 253.3m shares (305.8m with Greenshoe), reducing its stake from 73.5% to a current 36.4%. Whilst the initial market cap of Dr. Martens was £4.5bn, the price has collapsed 58% to under £2bn as of the time of this write-up.

Dr. Martens has several product categories:

Originals. These are the main focus and feature the classic, most recognizable, and iconic designs, like the 1460 and 2976 Chelsea boots. These products are meant to capture the essence of the brand and are merchandised on the Icon Walls in retail stores. Shoes in other categories are derived from them. 51% of FY22 sales.

Fusion. This line is much more alternative and disruptive, though it still builds on the DNA of Dr. Martens. These boots feature standout leather (and vegan alternatives), and thicker soles. Examples include the Jadon and Sinclair. 36% of FY22 sales.

Casual. Aims to attract those who wear athletic footwear and are not attracted to the above categories. 6% of FY22 sales.

Kids. Dr. Martens for newborns and children starting school. 4% of FY22 sales, with a large growth opportunity.

Accessories. Shoe related products like wax and laces, and other leather items such as small bags. 3% of FY22 sales.

The Group sold 14.1m pairs of its footwear in FY22 across EMEA (44% of sales), the Americas (42% of sales), and Asia (14% of sales) through D2C and B2B channels.

D2C (49% of FY22 sales compared to 26% in 2015) is comprised of e-commerce and retail. Dr. Martens operates websites that serve 12 countries in different languages, and e-commerce is a strategic focus, as it offers an extended product range and higher margins. Indeed, investments in digital transformation in the form of SEO optimization, increasing conversion rates, and a huge rise in value-adding projects as opposed to software fixes, have helped drive e-commerce sales and their mix from 7% of 2015 sales to 29% in FY22. For the medium-term, management is targeting a 40% ecommerce mix.

As to the retail component, the Group presides over 158 owned outlets spread across the globe. 80 are in EMEA, 41 in the Americas, and 37 in APAC. Management aims to build profitable stores with short breakeven periods of circa 2 years, small footprints, and short-term flexible leases (these often include rent payments as a percentage of sales and early tenant-only break clauses) in brand-appropriate locations. This cautious and profit-focused approach stems from the Group’s high sensitivity to retail dynamics and footfall pressures in its retail markets.

The retail stores are seen as brand beacons and offer the chance to try on products. Most have Icon Walls that showcase Originals and draw customers’ attention. I visited one in the Netherlands (I bought the 1460 Pascals and 1461 Monos) and can attest to the strong theme (it’s all black and yellow, with attentive staff and shiny leather everywhere). Retail contributed 20% of FY22 sales (mix stable since 2015), and management wants to maintain this 20% mix in the medium-term, with an annual rollout of 25-35 stores planned. Overall, the Group prefers the D2C channel because it affords greater control of the customer experience and brand image and is aiming for a 60% medium-term D2C mix (up 11% from FY22).

The B2B wholesale channel (51% of FY22 sales) covers multi-brand wholesale customers, distributors, and mono-brand franchise stores. The rationale behind wholesale partnerships is that they provide reach into geographies where the Group either does not have (or does not desire to have) its own distribution network or where the area to be covered is huge (as in the U.S.). As part of the professional transformation under Permira’s ownership (the PE investor became the majority shareholder in 2014), low-performing and underpenetrated wholesale accounts have been swapped for fewer, stronger, and strategic partners like Zalando who, for example, allow Dr. Martens to have a shop-in-shop and Icon Walls in their stores to promote the brand (they are brand custodians).

Partnered distributors and franchise stores prevail in those markets (Eastern Europe, Asia, and Latin America) where the Group lacks operating subsidiaries and are often converted into owned entities if desirable. Both distributors and franchisees often have brand exclusivity in a certain geographic region. The most recent conversions from distributor to Group-owned took place in Italy and Portugal. Whilst absolute sales growth is expected in the B2B segment in the medium term, the overall sales mix is expected to decline to circa 40% (down 11% from FY22 mix).

Dr. Martens manufactures its footwear in 14 factories across Vietnam (52%), Laos (22%), China (10%), Bangladesh (8%), Thailand (7%), and the UK (1%). These percentages represent Tier 1 production (direct suppliers) by share of total capacity, and recent years have seen a diversification of the supplier base, in particular a large reduction in sourcing from China. Dr. Marten’s products have low seasonality and fixed-price production contracts are agreed over 6 months in advance of a season, which helps to overcome continuing supply-chain snarls and provides cost visibility. In addition, whilst the Group has seen 6% cost inflation in the Autumn-Winter of 2022, this has been easily offset with price increases, with no impact on demand. I would wager this is because Dr. Martens’ footwear is well-known to be highly durable and good value-for-money. With rising energy costs and falling temperatures, investing in a solid pair of boots still makes sense.

The fragmented global footwear market was sized at £282bn in 2021, with around 10bn pairs sold. From 2014 to 2019, the market grew at a CAGR of 4.8%, with expected growth from 2021 to 2025 of 10% (pandemic recovery). As to the different categories within this TAM, leather footwear, which is Dr. Marten’s home turf, is the largest (33% of sales, 7% CAGR expected). Next are sneakers (16% of sales, 12% CAGR expected), athletic footwear (12%, 11% CAGR expected), and textile and other categories (39%). 81% of global footwear sales were offline in 2019, but online penetration has grown rapidly. In terms of the geographic revenue split for 2019, retail sales in EMEA were largest (34%), with Americas next (37%), and APAC (29%) last. In slight contrast, the Group’s own geographical FY22 revenue split indicates over-penetration in EMEA (44%) and under-penetration in APAC (14%).

Whilst Dr. Martens purchasers also wear other brands like Nike, Adidas, Vans, and Converse, there is much less overlap in the leather footwear space, and boots in particular.

Four pillars comprise management’s DOCS strategy:

D2C first. Growing through D2C e-commerce and retail channels grants control over how customers engage with the brand and expands margins. Easily observable KPIs are EBITDA margins, D2C mix, and store openings. This pillar is the most shareholder focused.

Organizational and operational excellence. This means striving to develop a strong culture with promotion opportunities (Dr. Martens has an excellent 4.1-star Glassdoor rating and started a share scheme for certain non-board members post-IPO), building a best-in-class, resilient, and sustainable supply chain, making technology a key business enabler, and improving organizational resilience and IT security.

Consumer connection. Revolves around communication with consumers and product strategy. Dr. Martens seeks to promote Rebellious Self Expression, and management wants to launch innovative, relevant products based on its icons, with leading sustainability characteristics. A digital marketing campaign is part of this pillar.

Support brand expansion with B2B. Partnering with fewer, better B2B partners to improve the brand’s presence. Also includes the conversion of certain markets if desirable.

Investment attributes.

The brand has been on the map for six decades and is one of the strongest in the footwear space. Dr. Marten’s shoes and boots are easily recognizable, durable, and their designs are timeless (Originals continue to drive sales). Few companies can rest on classic creations like the 1460 and 1461 and their derivatives for such a long period of time. Moreover, despite the brand’s historic association with the working class and specific youth cultures like punks, goths, rock, etc., Dr. Marten’s footwear appeals to a much broader, more vanilla consumer base.

Would I ever consider wearing the edgier Fusion line? No, the Originals are for me. But the width of the assortment is a great value-add. Desire for the unisex products also transcends gender, age, and income (average retail price in the UK is £109 to £189), with Dr. Marten’s purchasers represented across these variables in similar proportions.

"During the past seven years, the brand has been transformed in scale and professionalism, making Dr. Martens one of the most successful single-brand businesses in the world."

Tara Alhadeff - Partner at Permira and Dr. Martens Director

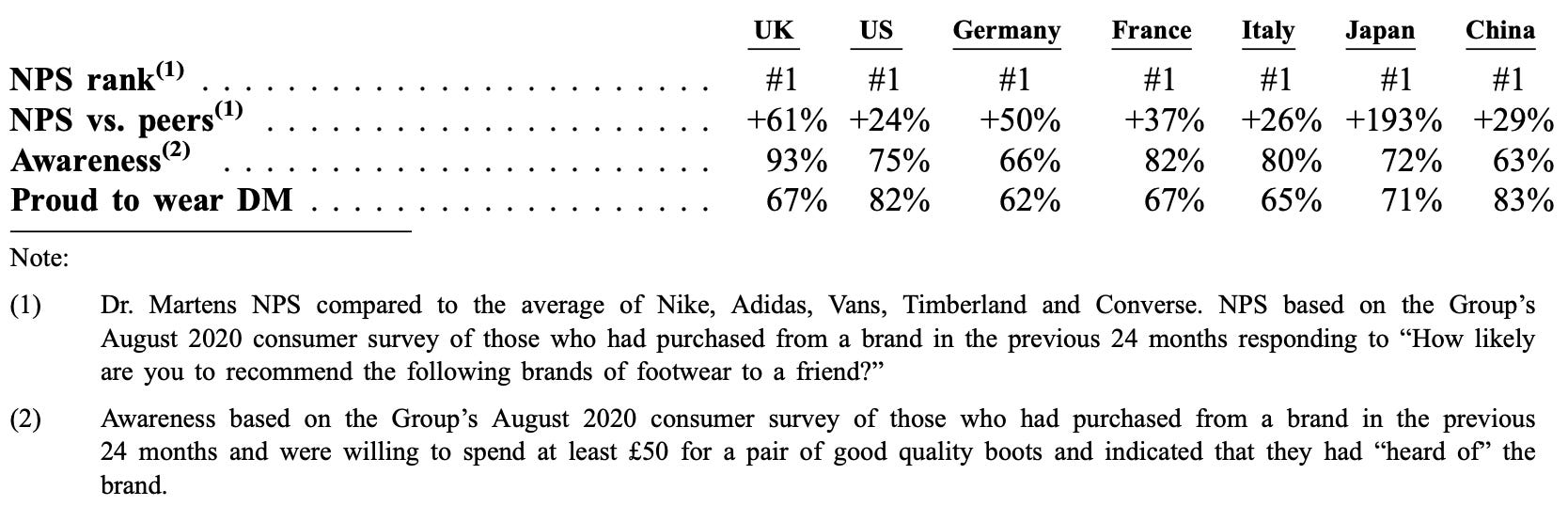

Loyalty to Dr. Martens is high and above market. Net promoter scores (% who would recommend the product) are the highest among peers (Adidas, Nike, Converse, & Timberland) and 60% of customers are considered repeat shoppers (not quite like recurring SAAS subscriptions, but still very good for a consumer brand, imop). The saleswoman at the Dutch retail store I attended (where I bought the 1461 Pascal boot and 1461 shoe, which are super comfortable and cool, again, imop) said that lots of older people return to purchase new pairs, which gels with the statistic that 72% of consumers who made a Dr. Martens purchase more than five years ago said they continued buying the footwear and 67% said they did not consider any other brand in their purchase decision. Bear in mind that these figures relate to the most penetrated UK market, but they still provide an indication of the company’s potential in other, under penetrated markets (Asian ones like China and Japan in particular).

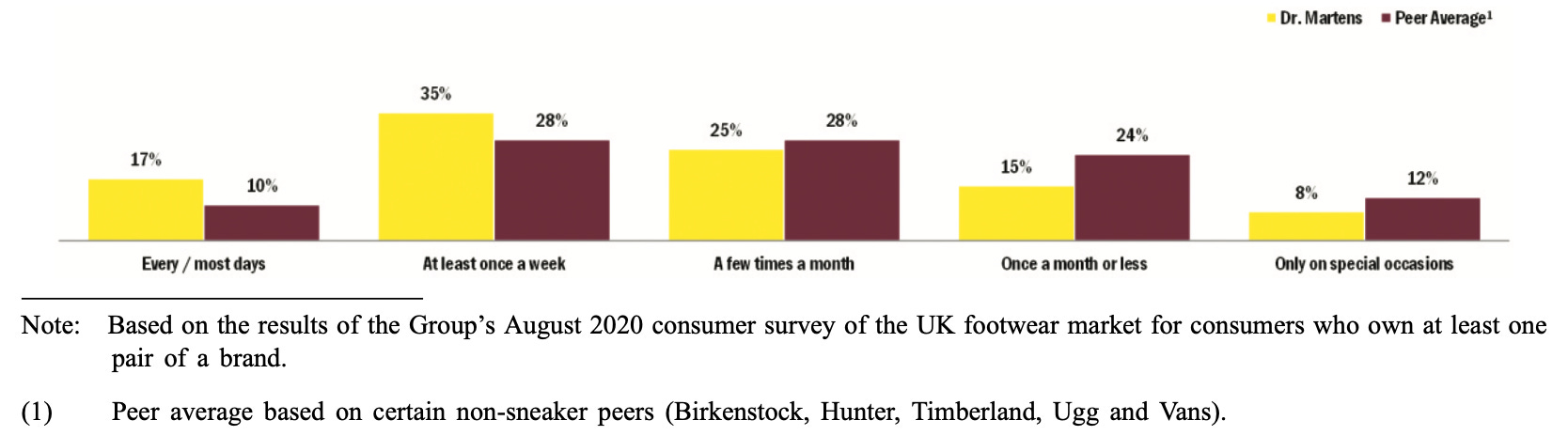

The five biggest wearing occasions for Dr. Martens owners are winter or bad weather, almost all occasions, going out at night, weekends and running errands, and going to concerts. For these wearing occasions, Dr. Martens’ products are significantly more popular than those of 13 peers (the likes of Birkenstock, Timberland, Hunter, Ugg, and Vans). About 1/5 consumers wear their Docs most days and 1/3 wear them at least once a week.

The strength of the brand also translates into a degree of pricing power; as mentioned, Dr. Martens has succeeded in passing on cost inflation to consumers with zero impact on volume (so far).

Besides the powerful brand, Dr. Martens also has a large market opportunity. Indeed, management estimates that there are 154m consumers across the UK, US, Germany, Italy, France, Japan, and China with similar attitudinal profiles as the circa 16m consumers who purchased Dr. Martens goods in the past year. Applying the current frequency and spend per purchase of the actual consumer base to this prospective population indicates potential sales of £6bn per annum (the largest opportunities by country are £2.7bn in China, £1.5bn in the U.S., and £0.5bn in Germany). Moreover, the market opportunity is likely significantly larger than this due to the aforementioned under penetration in certain markets. For example, in the most penetrated UK market, 32 boots are sold per 1000 capita compared to 17 in the U.S., 15 in Germany, 8 in Italy, 7 in France, 4 in Japan, and <1 in China.

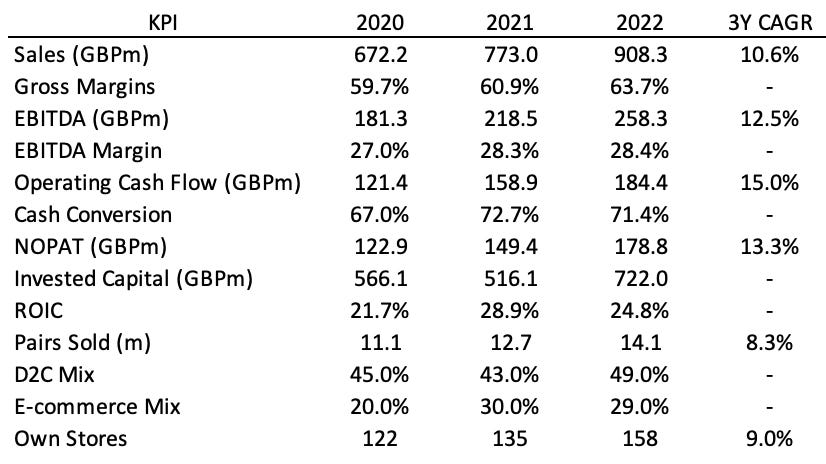

Management has executed well in the past, and this is reflected in the financial track record. Since 2015, Dr. Martens’ sales have grown at a 25% CAGR with EBITDA at a 37% CAGR. This increased growth of profits over sales can be attributed, of course, to the successful, ongoing, and industry-wide shift to D2C, which allows for better control over brand presentation and higher margins through e-commerce. Indeed, EBITDA margins rose from 17% to 28% in the same 2015-2022 period with the D2C mix up from 26% to 49% whilst the e-commerce mix increased from 7% to 29%. ROIC has also increased from 5-15% in the previous decade to 20-30% between 2020-2022. Permira retains its positive influence with a dominant 36.4% stake and a non-independent director, Tara Alhadeff, on the board since 2015.

Valuation.

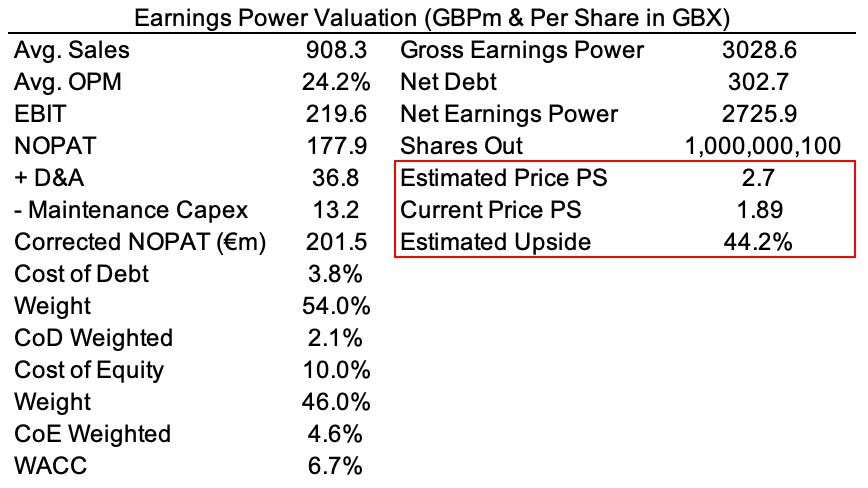

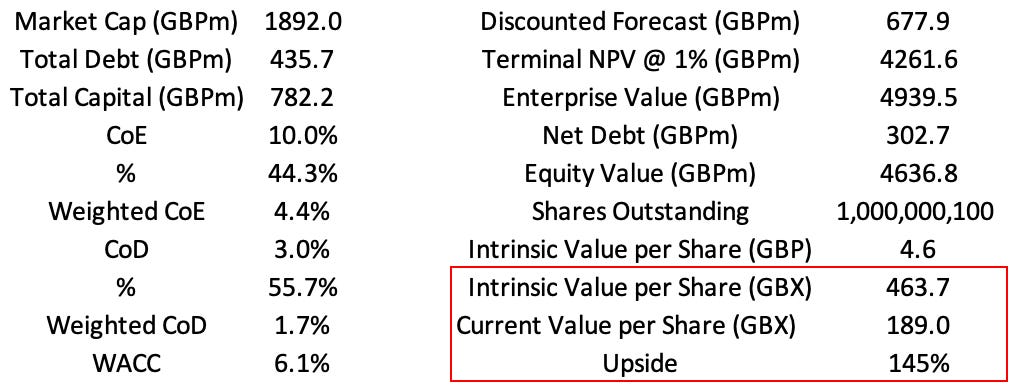

I used an earnings power valuation, which assumes a constant state of zero growth and excludes growth expenses, to estimate a worst case scenario for the Group. This produced a per share value estimate of 270p.

Of course, the earnings power valuation method is inappropriate because this firm has a strong growth element to it - in comes the DCF. I assumed mid-teens revenue growth as per management guidance; an effective tax rate of 21% for 2023 as per guidance and a 2024E increase to 27% due to the new, higher UK rate; a slight 0.25% increase in the net operating profit margin per annum to 21% in 2027, as higher margin e-commerce growth to hit the medium term mix target of 40% is expected but not certain. Additional assumptions include future capex of 3.5% (at the high end of guidance), CoE of 10%, CoD of 3% (middle of guided range) and terminal growth of 1%. To be clear, this is a base case, and I do not think the assumptions lean bullish at all.

The model and DCF output are shown below.

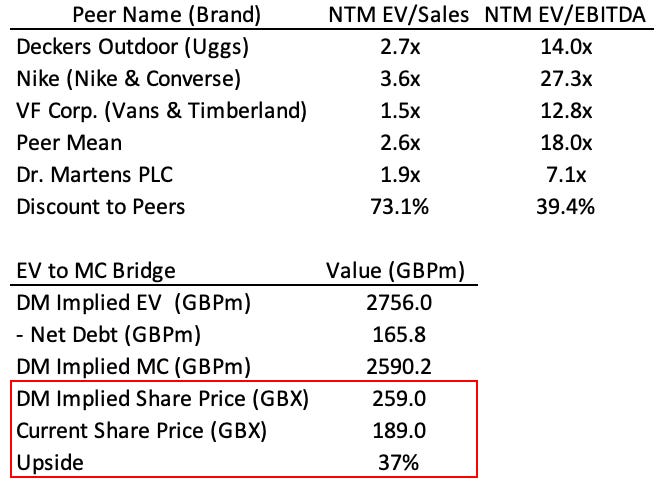

Dr. Martens peers are not single-brand companies, but a relative valuation is still useful. The below comps are all named in the IPO prospectus.

Whilst this valuation indicates far lower upside, the comps are poor. I also believe Dr. Martens should, in fact, trade much closer to Nike due to its strong and much more focused brand strength and similar e-commerce exposure (Nike has a 24% mix, DM has 29%). In that case, the price target rises to 365 pence (93% upside).

As an interesting aside, Birkenstock, another good comparator, was acquired by LVMH in Feb 2021 for €4bn, corresponding to 5.8x sales and 31x net income (FY19), or about three times Dr. Martens current valuation. At the same sales and earnings multiple, Dr. Martens would be worth about £5.3bn and £5.6bn, respectively. But we lack sufficient financial information here because Birkenstock was never public.

Risks.

I’ve read that some people think Dr. Martens is a fashion fad. There is a simple counterargument: what fashion fad grows sales at a 25% CAGR since 2015 with more than half of that revenue still coming from designs developed more than six decades ago?

Balance sheet debt.

Gross debt consists of £143m in capital leases and £296m in bank debt for a total of £439m.

Bank debt comprises a £300m term loan and £200m RCF. Both are due in Feb 2026 but the RCF remains undrawn.

Net debt is £306m. This seems manageable with around £421m in cumulative free cash flow expected between FY23 and FY25. But I would still like to see some active deleveraging to protect against a potentially large downturn.

Other information.

2023 remuneration for executive directors.

The bonus is 75% based on PBT and 25% strategic KPIs like employee engagement, sustainability, and brand equity.

The LTIP is 67% based on underlying EPS and 33% based on relative TSR.

The CEO and CFO made £1.7m and 930k, respectively, in 2022.

Insider ownership.

The CEO owns 1.1% (worth $26m) of shares and the CFO owns 0.8% (worth $18.4m).

Altogether, insiders own 38.6m shares, representing under 4% of the firm.

Possible reasons for the share price decline include general pessimism towards UK macro and markets (the FTSE250 is down 21% YTD) and the consumer sector in particular (recession fears).

The current dividend yield is 3.2% with a targeted payout ratio of 35% of net income.

Disclaimer: this write-up describes the author’s own research and opinions, and does not constitute investment advice, whether explicit or implied. Invest at your own risk and do your own due diligence. I hold a material position in the issuer’s securities.

Some other peers you might want to look at for your valuation. $CROX $SKX. Both trade at more similar valuations to $DOCS.L and have been growing. I also wouldn't comp to Nike, Nike is the golden standard when it comes to athletic wear brands.

I do think whenever you buy a fashion brand like this you need to worry about the fashion risk. I wouldn't think something like $DOCS.L is going to go away. But it's fashion ability and sales to go in waves.

Two pieces of data on this.

1) Google search trends look to be down this year compared to last for the important Holiday period. https://trends.google.com/trends/explore?date=all&q=%2Fm%2F0_sxs8v,%2Fm%2F064bsmc

2) When I went to my local mall for Christmas shopping the Dr. Marten's store was packed.

Thanks! My girl-friend says this brand is very popular now! Need to read and research!