Competition Demystified

Occam's razor applied to business strategy.

Understanding strategy and the types of real competitive advantages is crucial for all investors, that much is certain. Greenwald himself is something of a guru in the finance space, and now that I’ve read both his books on value investing and strategy, I think I’m qualified enough to judge that he more than makes up for his academic writing style with the clear frameworks and explanations that he provides. The various case studies are a particular highlight, and to be honest, they definitely make the book. Just don’t expect to be smiling ear to ear with each page.

Strategic Versus Tactical, And The One Force To Rule Them All

What is the difference between strategic and tactical decisions in business?

Strategic decisions are those whose results depend on the actions and reactions of rival companies. They’re made at the management and board level, consume corporate resources, are long-term in nature, and bring significant risk with them. Examples of strategic choices are which markets to enter, what critical competencies to develop, and how to fight the competition.

In contrast, tactical decisions can be made in isolation, without considering competitors, and their impact depends primarily on effective execution. Tactical decisions are typically short-term and are made at the middle and low levels of an organisation. They also have shorter timeframes and a limited risk profile. Common tactical questions might be how to incentivise sales staff, what discounts to offer for which products, and how to shorten delivery times.

Porter argued that five factors shape a competitive landscape in an industry: substitutes, suppliers, potential entrants, buyers, and competitors. However, Greenwald and Kahn break from this idea, and instead posit that one factor stands above all others in importance. That factor is barriers to entry, which make it very difficult for companies to enter a market and for incumbents to expand within it.

Conceptually, barriers to entry and competitive advantages are identical, as both describe the ability of a company to do something its rivals can’t replicate. And whilst tactical decisions are important in all situations, strategic decisions are exclusively relevant when barriers to entry exist, as the number of competitors in unprotected markets is too high to deal with effectively.

Types Of Competitive Advantages: Supply-Side

Supply-side competitive advantages are structural, and they allow a firm to deliver its products to the market at a lower price than rivals.

Cheaper inputs are a supply-side advantage. For example, Saudi Aramco has one of the lowest production costs per barrel of oil, in large part because Saudi Arabian oil is much closer to the surface than elsewhere, and conveniently pooled in large fields. However, though these lower costs do allow Saudi Aramco to be more profitable in a wider range of price environments, competitors aren’t kept out of the market. This holds true even if the market price per barrel falls below their relatively higher production costs, since these higher cost players would likely bear the pain for a while, hoping for better prices.

Proprietary technology in the form of product or process patents is another supply-side advantage. Pharmaceutical companies typically patent drugs, and industrial manufacturers might patent superior processes, like a method to produce extremely high purity metal. Other companies will have both types. However, the problem is that patents expire. This limits their benefits to a specific time period (often two decades), after which the barrier to entry disappears and must be renewed.

Simple learning and experience in industries with complex processes can also be a source of proprietary technology. The authors point out that semiconductor manufacturers, for example, often see their yields increase significantly over time through minor adjustments to their operations. If companies continuously exercise superior diligence in improving their processes, then they can outperform competitors for periods much longer than the duration of an average patent.

But technological change is an unrelenting force. If it’s rapid, then the optimised processes become obsolete as upgrades are necessary, which sends the company back to square one. And if the pace of technological change is slow, competitors are likely to catch up to an equivalent level of efficiency. It’s often a matter of time, as the authors confirm…

“In the long-run, everything is a toaster, and toaster manufacturing is not known for its significant proprietary technology advantages, nor for high returns on investment.”

With these significant limitations, supply-side advantages are considered the weakest of all.

Types Of Competitive Advantages: Demand-Side

Demand-side competitive advantages revolve around unique access to demand (customer captivity) in the form of habit, switching costs, or network effects.

Habit refers to a learned behaviour that is performed almost automatically. In a business sense, it often becomes relevant when repeat purchase, strongly branded, low-cost products are involved, like Pepsi or Marlboro cigarettes. However, this doesn’t necessarily mean that the power of habit extends to all such products. Beer drinkers will have a certain indifference to brands, and will likely order an Asahi instead of a Heineken in a Japanese restaurant. Similarly, most people don’t fuss about which toothpaste or disposable razor to buy at the supermarket. Also, let’s not forget that habit applies to a single product instead of an entire portfolio, which concentrates this advantage.

Switching costs are said to be high when it takes significant time, money, and effort to replace the current supplier of a product. For example, a significant proportion of banks still use software based on the 1960s COBOL programming language because the data risk and headache of upgrading is so high (if it ain’t broke, don’t fix it). Likewise, surgeons will need to see proof that a product is far superior on all dimensions before committing to the required training and introducing it into their operating theatres. They must also consider the extremely high cost of equipment failure in the form of disability or possible death of a patient. In contrast, standardised products often have little or no switching costs, endearing them to consumers.

I believe that network effects, which increase the value of a product or service with each new user, are also a huge demand-side advantage. They’re most obvious for social platforms like LinkedIn and online marketplaces like Etsy, where the winner takes the entire cake for himself.

Overall, demand-side competitive advantages are more common and robust than supply-side advantages. But they’re certainly not immune from erosion. Today’s customers move elsewhere, change interests, and do not live forever, whilst tomorrow’s are unattached and equally available to all industry players.

Types Of Competitive Advantages: Economies Of Scale

Economies of scale are perhaps the most classic competitive advantage. As production increases, the cost per product unit decreases, since fixed and variable costs are spread over a larger number of units.

The strength of this advantage depends on the size difference between a firm and its rivals in the form of market share. The larger the difference in market share, the wider the moat, as the major firm can sell its products at a lower price with equal or higher profitability, or at an actual profit when others make losses. Of course, a high percentage of fixed costs is ideal, since this results in the most scalability. Software publishing is an example of a model where costs are overwhelmingly fixed.

But economies of scale alone are not enough, since efficient rivals with equal access to customers and common costs can still establish an identical level of scale over time. What’s required to sleep well at night is a degree of customer captivity combined with scale economies, because this ensures that the bigger firm maintains its market share even if smaller, eager rivals match it on price and other product features.

“With some degree of customer captivity, the entrants never catch up and stay permanently on the wrong side of the economies of scale differential. So the combination of even modest customer captivity with economies of scale becomes a powerful competitive advantage.”

Of course, economies of scale need to be defended, and the best strategy for an incumbent with economies of scale is to mirror the moves of an aggressive rival to secure its market share (it is relative size, not absolute revenue, that creates scale). This might involve matching price cuts and product launches. Conveniently, the costs of the entrant will be higher at each stage of such a struggle. In other words, both players bleed, but the entrant much more so than the incumbent. Making customers more captive is also important.

Large markets are a problem for firms with scale economies because they attract a high number of competitors, all of whom are itching to capture market share. It’s best to operate in a small niche. But fast-growing markets are also a liability. The reasons for this are that the new customers who drive such markets are first of all not held captive - a prerequisite for a long-term scale advantage - and that the scale effect itself is under threat of erosion. The below table demonstrates how scale economies can fade in quickly growing markets.

The first segment represents the original market, where there is a 16% difference in fixed costs as a proportion of sales between the entrant and incumbent. In the second segment, the market and firm revenues are doubled in size, and the difference halves to 8%. In the final segment, where the market and revenues are 10x the original, the difference in fixed costs as a proportion of revenue drops to a mere 2%.

This mathematical relationship shows that economies of scale are easier to defend in slow-growing, mature markets, like those of alcoholic beverages, commercial aircraft manufacturing, and soda production.

“Although it may seem counterintuitive, most competitive advantages based on economies of scale are found in local and niche markets, where either geographical or product spaces are limited and fixed costs remain proportionately substantial.”

This quote emphasises the importance of thinking locally when it comes to economies of scale. As an example, the authors point to Coors, a beer producer headquartered in Colorado. Back in 1975, Coors was available in 11 states, and it boasted double the net margin of Anheuser-Busch (AB) when it went public that same year. Coors was extremely vertically integrated, operated a single, massive brewery, and didn’t pasteurise its beer. Its local economies of scale in advertising and distribution - major costs that are more or less fixed on a regional basis - were huge.

But following an FTC ruling that accused it of restricting distribution, Coors decided to go national. Consequently, its economies of scale dissipated and its margins shrank. Its operating income per barrel slipped from $8.5 in 1977 (AB had $4.6) to $6.3 in 1985 (when AB reported $11.4), as COGS and in particular advertising costs exploded. A similar thing happened to Walmart when it decided to expand outside of the regions in which it was dominant.

Identifiying Competitive Advantages

What is most interesting to us as investors is how to identify whether a company has some sort of competitive advantage. For this, the authors suggest the following process.

First, it helps to construct a simple industry map that shows where the company operates in the wider value chain. What market is it in, and who are the competitors? If the list is long, that’s a bad sign.

Second, we need to look into market share. Has it remained remained stable over time? If so, this indicates a defensible position and a competitive advantage. Boeing and Airbus, for instance, have given and taken a few percentage points of share from each other in the past decade, but overall, the narrow-body and wide-body airliner markets are insulated and duopolistic.

Third, what do operating margins and after tax returns on invested capital (NOPAT/IC) look like? Companies with advantages should theoretically have higher margins than their competitors and be able to earn returns significantly above their cost of capital. Average ROIC values in the 15-25% range over a decade typically indicate an advantage, whereas those in the 6-8% range point to their absence. What’s important here is to adjust for possible dilution in the consolidated reports; whilst an advantage might exist in a particular segment or a certain product space or geography, this can be diluted at the level of parent reporting.

If the second and third tests check out, then we can be quite certain that an advantage exists. The next step is to identify what type of advantage it is, which requires that we work from the general category to the specific factor that protects the company from competition. Let me point out a few accessible examples…

Microsoft benefits from economies of scale in PC operating software, and high switching costs because it takes people a long time to become proficient with their productivity software.

Cigarette manufacturers like British American Tobacco and Altria boast massive economies of scale and perhaps the strongest possible customer captivity through the legal but addictive ingredient that is nicotine.

Proprietary technology in the form of product and process patents was crucial to the commercialisation of BioNTech’s COVID vaccine.

What If There Is No Competitive Advantage?

Companies which have no advantage should focus on efficiency above all else, and should expect to earn their cost of capital. Such firms are not necessarily unattractive candidates for investment, as running a tight ship can sometimes produce significantly better fundamentals than those of competitors.

But they certainly do require more vigilance on the part of investors and management alike than “wonderful companies” like Coke, which can be left to compound over decades and have so far seemed to reward long-term investors who practice adaptive laziness.

“I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.”

Warren Buffett

Using Game Theory To Understand Strategic Decisions

Greenwald and Kahn provide a short but useful discussion of a fictional decision on the part of Lowe’s to open a store on the so far untouched turf of Home Depot, a fierce rival. I think it brings home the complexity and difficulty of predicting the net effect of even simple strategic decisions.

To demonstrate, in the above scenario, Lowe’s would be concerned about what Home Depot is likely to do, which depends on how Home Depot interprets its actions. This interpretation, in turn, depends on how Lowe’s has acted in the past, how it reacts to Home Depot’s behaviour, the signals that Lowe’s sends, and Home Depot’s own perspective on business imperatives, which depend on its culture. Of course, all of these factors apply equally to Lowe’s reading of Home Depot’s signals, and on Lowe’s own culture. The confusion is real…

“There is the danger here of infinite regress, reflecting mirrors ad infinitum. To bust out of this trap requires a clear focus and some useful simplifying assumptions.”

Fortunately, most competitive interactions revolve around either price or volume. This makes the theory much easier to understand. If two companies offering the same product charge a high price, they earn high profits, and split the market equally. If they both charge low prices, they earn low profits, and again split the market between them. But if one charges a high price and the other a low price, then the one that sells for less should see its profit surge, provided that the increase in volume exceeds the decrease in price per unit. The competing company is left stranded at a higher price with lower absolute profit, unless it chooses to drop its prices as well.

This situation is known as the prisoner’s dilemma game, since it mimics what two criminals would go through if interrogated separately. If they cooperate, they will face a light sentence. If they both confess, they will also see little time in prison. But if one confesses and the other maintains his innocence, the latter will be in the worst situation possible. Essentially, there is a powerful incentive to abandon the group interest and confess, since this results in less prison time and avoids the possibility that the other criminal leaves you hanging. The usual outcome of a prisoner’s dilemma is the “non-cooperative equilibrium”, which in this classic scenario would be that both confess.

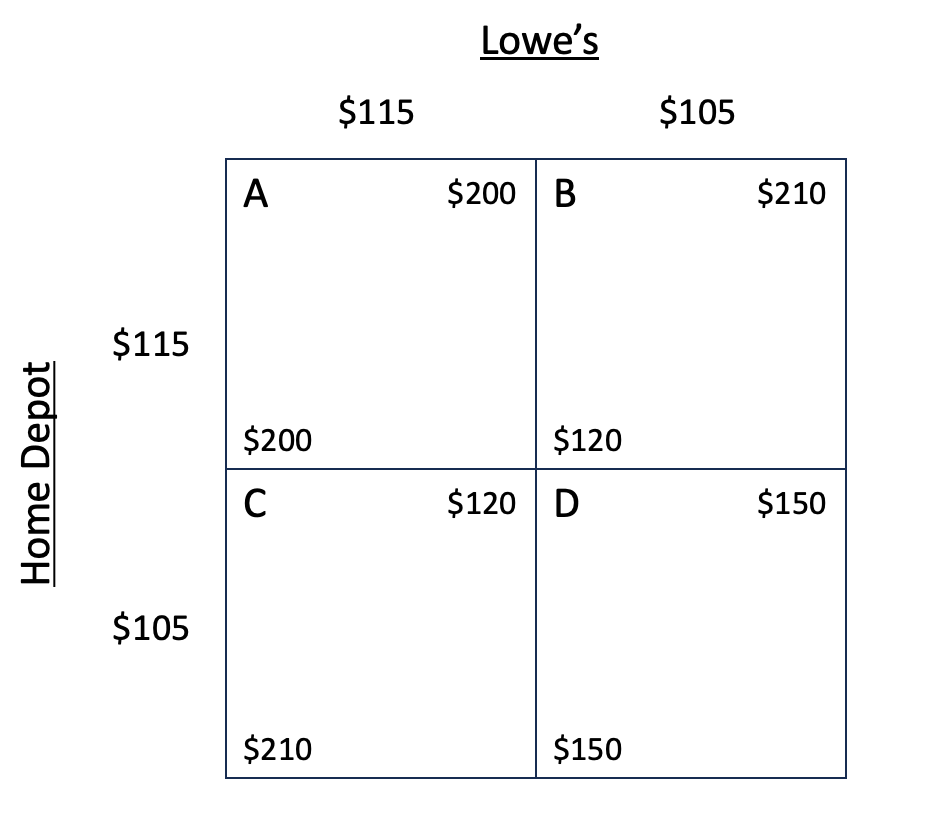

To represent a simple product pricing decision, we would use the below matrix. $115 or $105 are the price choices that each firm can make, whereas the numbers in the boxes represent the outcomes for each (top-right for Lowe’s, bottom-left for Home Depot). For example, if Lowe’s charges $105 but Home Depot continues to charge $115 (Box B), then Lowe’s makes $210 in profit compared to $120 for Home Depot. The assumptions here are a $75 COGS and either an even 5 and 5 customer split if the decisions are identical, or a 7 and 3 split of customers if not, for a total of 10 customers in the market.

What’s most obvious in the above matrix is that cooperation at the $115 price level produces the highest gross profit for both companies. Logically, shouldn’t they cooperate? But the strong temptation to deviate is ever present, both to gain an advantage and avoid a disadvantage if the other acts first, and it is also naïve to assume that profit is the ultimate motivator for all companies. For example, relative performance might be emphasised in a firm’s culture. Thus, in both theory and practice, the normal outcome is that both companies charge the lower price of $105. This state is described as the “Nash equilibrium”, and it depends on a pair of conditions…

Stability of expectations. Each competitor believes that the other will maintain its position among all other possible choices.

Stability of behaviour. Because expectations are stable, neither rival can improve its position with different behaviour.

How can this detrimental equilibrium be avoided? Through certain structural adjustments. These include…

Avoiding direct product competition, which can remove duplicative overhead and enhance economies of scale.

Designing and implementing strong customer loyalty programs. Rewards should be cumulative instead of current, and the rate of reward accumulation must rise with increasing volume. These factors are crucial because they differentiate the program from a general price discount.

Limiting output capacity. If a potential deviant can’t keep up with the additional volume it would gain, then the incentive to break from the status quo is weak. This does require cooperation on the part of all rivals, and barriers to entry.

Most-favoured nation pricing policies. These dictate that if a firm offers a lower price or better terms to a single customer, it must put the same offer to all of them, ensuring that the costs of acquiring new business outweigh the gains.

Changing management incentives from ones that emphasise sales growth and relative performance to profitability alone.

The authors point out that tactical choices can also help to avoid the lose-lose Nash equilibrium in a price and volume war. Specifically, firms should respond immediately to price reductions, and simultaneously signal a willingness to return to higher prices. Deviant but rational managers, after a few rounds of fruitless sparring, should realise that unofficial cooperation produces the more favourable outcome.

The prisoner's dilemma is but one example of how game theory can be used to understand simple strategic decisions. Though the authors also provide an analysis of market entry decisions and industry cooperation, these are far outside the scope of this post.

What I thought was best about this book was the framework for identifying competitive advantages, the various case studies (Coke and Pepsi, Coors, Polaroid and Kodak), the importance of local thinking when it comes to scale, and how the authors smoothly impressed the complexity of strategic decisions on me. For those who are less inclined to read the entire book, I’d recommend Greenwald and Kahn’s shorter article in the Harvard Business Review, which still covers some interesting points and provides a concise discussion of the true source of Walmart’s competitive advantage.

Great summary! Thanks